By Syndication Washington Post, Bloomberg · Vildana Hajric

U.S. stocks pulled back from record highs, with small-cap shares posting their biggest drop in a month, as prospects faded for bigger government aid checks to individuals. The dollar weakened.

The Russell 2000 Index tumbled almost 2%, while the S&P 500 finished only slightly lower. A gauge of global equities was set to close at a record after the U.S. House backed President Donald Trump’s proposal to boost aid checks for individuals, but pulled back from its high of the day as Senate Republicans blocked an attempt by Democrats to increase the direct payments to $2,000 from $600.

The year is coming to a close with risk assets such as stocks, corporate bonds and bitcoin just off record highs. As investors try to gauge the impact of the pandemic and the pace of U.S. vaccine distribution, the S&P 500 is set to end the year 15% higher.

On the coronavirus front, more restrictions are being imposed to fight the spread of the new, more infectious strain. covid-19 hospitalizations in the U.S. reached new highs, while Southern California plans to extend a regional stay-at-home order. South Korea’s daily toll of fatalities rose to a record, while Thailand reported its first virus death since November.

In Europe, the Stoxx 600 rose as the FTSE 100 Index rallied in the first session since the U.K.’s Christmas Eve trade deal with the European Union. Uncertainty about what accord will be struck on financial services weighed on Lloyds Banking Group Plc, Natwest Group Plc and Barclays Plc.

Elsewhere, the pound recouped some of Monday’s decline.

These are the main moves in markets:

Stocks

– The S&P 500 Index fell 0.2% as of 4 p.m. EST.

– The Stoxx Europe 600 Index gained 0.8%.

– The MSCI Asia Pacific Index jumped 1.4%.

– The MSCI Emerging Market Index increased 1.1%.

Currencies

– The Bloomberg Dollar Spot Index sank 0.4%.

– The euro increased 0.3% to $1.2249.

– The British pound gained 0.4% to $1.3499.

– The Japanese yen strengthened 0.3% to 103.53 per dollar.

Bonds

– The yield on 10-year Treasuries rose one basis point to 0.93%.

– Germany’s 10-year yield dipped less than one basis point to -0.58%.

– Britain’s 10-year yield fell four basis points to 0.21%.

Commodities

– West Texas Intermediate crude gained 0.8% to $47.99 a barrel.

The Eastern Economic Corridor (EEC) Office has maintained its target of investment in the EEC zone over the next three years at Bt100 billion, despite the gloomy global economic outlook.

Meanwhile the number of investors granted EEC promotion certificates in the first 11 months of 2020 rose 62 per cent, indicating investors are confident to continue investing, said Luxmon Attapich, the office’s deputy secretary general for Investment and International Affairs.

In 2021, the EEC will focus more on wooing investment from industries benefiting from the Covid-19 pandemic fallout, including the digital, health and logistic businesses.

During the first 11 months of 2020, total investment in processed food, the bio-industy and medical industry stood at Bt18 billion, which is expected to rise 70 per cent in the next three years.

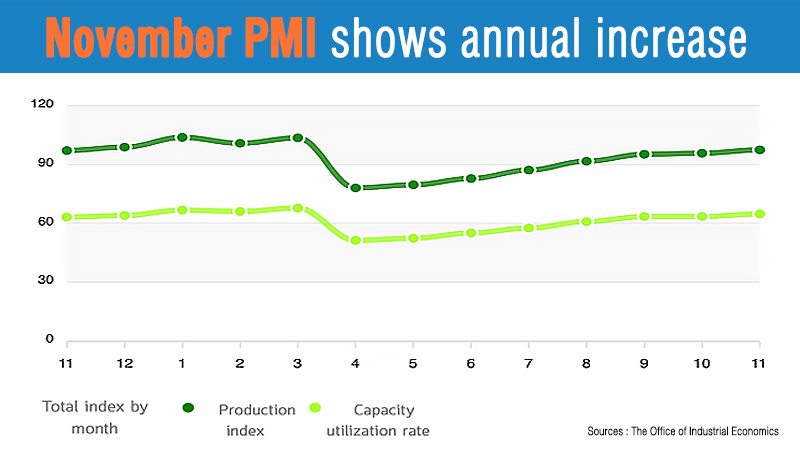

Thailand’s manufacturing production index (MPI) rose 0.35 per cent in November from a year earlier, for its first annual increase in 19 months.

The index also rose 1.77 per cent from last month driven by a 10.2 per cent growth in auto manufacturing, said the Industry Ministry.

The figures showed Thai manufacturing was on the path to recovery after being hit by the trade war and Covid-19 outbreak, said Thongchai Chawalitpichaet, director-general of the ministry’s Office of Industrial Economics.

Global economy recovery aided by stimulus packages had boosted orders for Thai-made products, resulting in a smaller export contraction of 0.87 per cent last month, he added.

He expects December’s PMI to match November’s level, if authorities can contain the latest virus outbreak.

Overall in 2020, the PMI is expected to contract by 8 per cent but then grow by 4-5 per cent next year, he said.

The manufacturing sector is expected to contract 7 per cent this year, then expand 4-5 per cent next year, based on an exchange rate of Bt29-32 per dollar and crude oil at US$40 to $50 per barrel, he added.

Kasikorn Asset Management (KAsset) expects the Stock Exchange of Thailand (SET) Index to move between 1,550 and 1,600 next year amid the global economic recovery.

KAsset managing director Suradech Kietthanakorn said Thai bank, energy, petrochemical, hotel and healthcare stocks will benefit from the recovery, while the performance of shares in public utilities, retail, public transport and electronics shares should improve next year.

He added that positive sentiment from Covid-19 vaccines, central banks’ moves to ease monetary policy, and countries’ economic stimulus measures is driving the SET upwards.

“However, investors should diversify risks and invest with caution due to impacts from Covid-19, domestic politics, US-China relations and President-elect Joe Biden’s administrative policies.”

He advised investors to consider the K Global Income Fund (K-GINCOME), K Global Income Fund-SSF (K-GINCOME-SSF), K China Equity Fund (K-CHINA) and K China Equity RMF (KCHINARMF).

The Thai Hotels Association (THA) will ask for more government measures to soften the impact of Covid-19 on the sector, THA chairperson Marisa Sukusol told the Thansettakij newspaper.

Among them is a measure allowing hotels to suspend their outstanding debt. Hotels want to halt their principal and interest payments for two years. The THA also wants annual interest on hotel debt to be cut to 2 per cent.

The THA will also ask the government to allocate budget for soft loans of up to Bt60 million per hotel at 2 per cent interest, with principal and interest repayment suspended for two years. When payment is due, the loans should be converted into long-term credit at low interest. The loans were needed to boost liquidity, the association said.

It will also ask the government to pay 50 per cent of monthly staff salaries in order to retain as many as 200,000 hotel employees nationwide.

The co-payment scheme would cover monthly salaries of up to Bt15,000 and last for one year. Payments would be transferred directly into their accounts via Krungthai Bank. The total cost of the scheme is estimated at Bt18 billion.

Hotel operators calculate the Covid-19 impact could drag on until late next year, due to the fresh outbreak in Thailand.

The new surge of infections has seen some hotels that had reopened, close again after guests cancelled bookings over infection fears.

By Syndication Washington Post, Bloomberg · Laura Davison

Unemployed people claiming federal benefits won’t see a one-week gap in their payments despite the delay in President Donald Trump signing the program extension into law, according to the Department of Labor.

States are implementing the provisions as quickly as possible, and the Labor Department doesn’t anticipate that claimants will miss a week of benefits due to the timing of the new law’s enactment, a spokesman for the Department said in a statement Tuesday.

Trump signed a bipartisan stimulus and government funding bill, which included an 11-week extension of unemployment benefits, into law on Sunday, a day after benefits expired. That prompted concern that jobless Americans would lose out on benefits for the last week of December. Trump held off signing the bill for several days as he demanded bigger stimulus payments for individuals and action on two unrelated issues involving election security and removing a liability shield for technology companies.

The pandemic relief law provides a $300-a-week payment for jobless individuals and extends benefits for self-employed and gig workers through mid-March. The $300 federal payments are on top of benefits that state unemployment offices provide. The state benefits vary by income and jurisdiction, but the average state payment was $378 a week, according to Labor Department data.

The measure largely extends programs with few changes, meaning that existing guidance will continue to apply, making it easier for the states to implement, the Labor Department spokesman said.

“Millions of jobless workers will be able to breathe a sigh of relief, knowing that they will not lose a week’s worth of income,” Oregon Sen. Ron Wyden, the top Democrat on the Senate Finance Committee, said in a statement. “Now, Donald Trump’s needless delay in signing the relief bill still means unnecessary administrative headaches and late payments, but workers will not lose income.”

About 14 million Americans have been receiving benefits under the Pandemic Unemployment Assistance and Pandemic Emergency Unemployment Compensation programs extended in the law.

The uninterrupted jobless benefits could help bolster the economy that has struggled as consumer spending has been falling and unemployment claims remain at elevated levels.

Consumer spending, which accounts for a majority of the economy, dropped 0.4% in November — the first decline since April, according to Commerce Department data. Personal income decreased 1.1%, reflecting the winding down of several pandemic aid programs.

By Syndication Washington Post, Bloomberg · Christopher Condon

The Federal Reserve has delayed the termination of the Main Street Lending Program to Jan. 8, from Dec. 31, in order to finish processing loans submitted by a Dec. 14 deadline to tap its funds.

The extension was approved by the secretary of the Treasury, the Fed said in a statement Tuesday.

The Treasury Department provoked controversy in November when it ordered the Fed to close Main Street and some other emergency pandemic lending programs by Dec. 31. Secretary Steven Mnuchin said the order was driven by lawmakers’ intent when they crafted the Cares Act in March, legislation that provided taxpayer money to support the programs. The Fed had asked that they all be extended into 2021.

Main Street has struggled to live up to its initial promise, although borrowing picked up somewhat as the deadline approached and stood at $14.5 billion as of Dec. 23. The program was designed to provide as much as $600 billion in credit to mid-sized U.S. companies damaged by covid-19.

Brexit deal offers scant solace to City of London under threat

InternationalDec 30. 2020The City of London. MUST CREDIT: Bloomberg photo by Jason Alden

By Syndication Washington Post, Bloomberg · Viren Vaghela

The trade deal that both sides of the English Channel say reflects a new era of cooperation is essentially a sideshow for the City of London, which is still awaiting its own seal of approval from the European Union.

EU officials must rule separately that British financial regulations and oversight are strong enough to create a level playing field. Without that, a steady leakage of business – already underway in some areas – may become a daily reality for the U.K.’s finance industry.

Boris Johnson has already said in an interview with the Sunday Telegraph that, when it comes to financial services, the treaty “perhaps does not go as far as we would like.” Chancellor of the Exchequer Rishi Sunak said that discussions with Brussels over access for financial services will continue.

While there’s been progress in preventing Brexit from upending financial markets in the short term, there’s little consensus on the ultimate nature of the U.K. finance industry’s relationship with the EU, just days before it loses much of its longstanding access to the bloc.

“The dangerous bit is that you are seeing people moving assets, moving trading books to other locations,” Howard Davies, chairman of NatWest Group Plc, said in a Bloomberg Television interview this month. “The risk is that as that happens, then the staff follow over time.”

The hope among British bankers, regulators and politicians is that the trade deal helps unlock a separate agreement for finance. The industry is a key pillar of the U.K. economy, employing more than 1 million people and accounting for more than a tenth of all tax revenue.

“While a deal is welcome, financial and related professional services are clear-eyed about the need for both sides to continue to develop the relationship in services,” said Miles Celic, chief executive officer of TheCityUK, representing Britain’s finance hub.

Likewise, bankers in Europe are eager for clarity. The Association for Financial Markets in Europe, one of the region’s biggest industry lobby groups, called for an agreement on “equivalence” decisions which would smooth cross-border financial market access.

“We hope that this lays the foundation for further cooperation on financial services,” said Adam Farkas, AFME’s CEO. “It is important that the EU and the U.K. now urgently put in place outstanding equivalence decisions to mitigate disruption at the end of the transition period and ensure a smooth adaptation to the new relationship.”

Still, even the most optimistic financiers concede that the status quo, with London as the financial hub for an entire continent, is unlikely to hold.

European Commission President Ursula von der Leyen has vowed “all will change” in the City of London’s relationship with the EU. And in a sign of what’s to come, Bank of France Governor Francois Villeroy de Galhau warned Europe’s banks in October to prepare for a longer term shift away from using London clearinghouses, which underpin the multi-trillion dollar derivatives markets.

It goes “back to this core and fundamental question of where Europe wants to have its center of financial activity,” Mairead McGuinness, European commissioner for financial services, told Euronews in December. “It certainly will not, in the long term, continue to be the City of London.”

The Goldman Sachs offices in London. MUST CREDIT: Bloomberg photo by Jason Alden

With Britain suffering its worst recession in more than three centuries, it can ill afford damage to the finance sector that paid about 75 billion pounds ($100 billion) in tax in 2018.

Despite that, financial services garnered little of the attention bestowed on fishing in the trade talks, even though every fisherman in the U.K. could fit in the City of London’s latest office tower.

“Nothing against fishermen, and I eat a lot of fish, but nonetheless the financial sector is a larger share of the economy than the fishing sector and yet we hear nothing,” Davies said in an October interview.

Companies including JPMorgan Chase & Co. and Goldman Sachs Group Inc. have recently started to shift more business to the bloc. The moves, which for JPMorgan included 200 billion euros ($230 billion) in assets and 200 staff, are just the “first wave,” Dorothee Blessing, the head of the firm’s Frankfurt unit, said in September.

Non-German lenders are in the process of moving 397 billion euros of holdings to Germany, taking their combined balance sheet there to 675 billion euros at the end of the year, the Bundesbank said in a presentation to reporters at the start of November. The European Central Bank has said banks have agreed to ultimately move a total of 1.3 trillion euros of assets to the euro area.

Elsewhere, more than half of stock trading in London is in shares of European companies and may migrate to EU venues. Last month, The 300-year-old London Stock Exchange Group Plc joined other trading venues in opening a platform in the EU because of the absence of a deal for finance.

For now, London has hardly been hollowed out and it holds formidable advantages that will take years, if not decades, to erode. Plenty see an opportunity for the City of London, whose global stature is testament to its long history of adaptation.

“London will reinvent itself to remain a hub,” said Ali Jamal, founder of wealth manager Azura, which has an office in Mayfair and manages about $3 billion. “No city in Europe can compete with London on three factors: language, legal system and infrastructure.”

Still, it has been hard preparing for a future that is both murky and very complex. The government arranged a webinar for finance firms in October, with a pre-recorded speech and slides on topics such as accounting, emblazoned with the branding “U.K.’s new start, let’s get going,” according to one attendee who asked not to be named. The content was too general to be useful, the person said.

The trade deal offers some certainty to the broader economy, which will indirectly help the banks. “Reaching a trade deal is important for our corporate clients as they will want to avoid the impacts of tariffs on cross border trade in goods,” said James Bardrick, head of the U.K. at Citigroup Inc.

And the deal may also help unlock what Bardrick and his peers want most: an EU declaration that U.K. regulations are robust, known as equivalence. This ruling would enable business to continue largely as usual – but it’s in the hands of the EU, which can also withdraw equivalence at short notice.

Over the long haul, much will depend on the course of political horse-trading for finance and what regulators and supervisors expect, according to Citigroup’s Bardrick. “We and the rest of the industry may need to evolve our plans and staffing levels to serve our clients in Europe effectively,” he said.

It’s that lingering uncertainty that is set to define the City of London’s future even as the U.K. begins to negotiate trade accords in earnest.

“Four years ago a nation decided to shoot itself in the foot and see if it could run a race,” said Michael Mainelli, executive chairman of finance consultancy Z/Yen, who was elected sheriff of the City of London in 2019. “Brexit is an unnecessary distraction. Nobody has shown me a single advantage economically in any shape or form.”

IPOs in Japan enjoy popularity not seen since the dot-com bubble

InternationalDec 30. 2020Visitors look at an electronic ticker at the Tokyo Stock Exchange on Oct. 29, 2020. MUST CREDIT: Bloomberg photo by Kiyoshi Ota

By Syndication Washington Post, Bloomberg · Shoko Oda, Ayaka Maki

In a surprisingly strong year for initial public offerings globally, Japan’s 2020 market debutantes enjoyed their best opening share performances since the dot-com bubble era, helped by a groundswell of retail investors hungry for tech issues.

The average initial pop for IPOs in the Japanese market this year was nearly 130%, the most since 1999. The best performer was artificial-intelligence systems firm Headwaters Co., which jumped 1,090% in its first trade. Image-recognition software maker Ficha Inc. came second with an 806% gain, followed by internet-of-things developer Tasuki Corp., which rose 655%.

Backed by easy-money policies and growth in individual investing, new listing markets have been frothy this year despite the coronavirus market turmoil, as seen in the dramatic gains of Airbnb Inc. and DoorDash Inc. in U.S. debuts earlier this month. Stay-at-home tech plays and cloud computing upstarts especially found 2020 to be the perfect time to tap the public markets.

“The reason for the large opening gains is that there were many IPOs of stocks that were relevant to the times,” such as Japan’s digitalization push, said Hideyuki Suzuki, a general manager at SBI Securities Co. With low interest rates expected to continue for some time, the IPO market should continue to attract funds, he said.

Japanese stocks overall lagged in the pandemic recovery, with the Topix not erasing its year-to-date loss until November, months after U.S. and Asian peers. The Tokyo Stock Exchange’s Mothers Index of start-ups was a notable exception, with a gain of around 30% on the year, thanks to its heavy weightings of biotech and Internet names, as well as the surge in retail investing.

A total of 94 companies went public in Japan in 2020, up by four from the previous year, even with a pandemic-driven drought from early April to late June. About 70% were listed on Mothers. The overall value was small, with firms raising a total of $3.3 billion, and no single deal worth more than half a billion dollars. That compares with $181 billion raised in the U.S. and $51 billion in Hong Kong.

Toshiba Corp.-affiliated chipmaker Kioxia Holdings Corp. in September decided to postpone what would have been Japan’s largest offering of the year, at up to $2.9 billion, due to market uncertainty amid U.S.-China trade friction. That made mushroom cultivator Yukiguni Maitake Co., which raised $409 million, the biggest Tokyo IPO of 2020, followed by musical instruments maker Roland Corp. and business consulting provider Direct Marketing Mix Inc.

In the absence of blockbuster deals with international appeal, local retail traders helped pick up the slack. Individuals accounted for 20% of total trading value on the Tokyo Stock Exchange this year, up from about 16% in 2019.

“IPOs have helped drive retail investor turnover,” said Shoichi Arisawa, an analyst at Iwai Cosmo Securities Co. “It’s helped money come back to growth stocks and given life to the start-up market.”

In 2021, investors will be watching whether Kioxia decides to try its luck again. So far one company has announced IPO plans for next year, with laser-based chip solutions firm QD Laser Co. planning to list in February.

Doctors and nurses across Britain are sounding the alarm as confirmed cases of covid-19 reach record highs, with experts urging the government to implement a stricter lockdown to prevent the health system from being overwhelmed.

Simon Stevens, chief executive of the National Health Service (NHS) in England, told reporters on Tuesday that hospitals were “back in the eye of the storm” as new cases surged across Europe and Britain. He said more must be done to ease the burden on health-care workers.

Some health-care workers are issuing their own public warnings, detailing how hospitals in London and the southeast of England are already setting up tents to increase their capacity. They say ambulances are waiting outside hospitals for hours because there is no space inside.

“Our control room staff are having to make incredibly difficult decisions to decide who gets an ambulance first and who they are going to ask to wait,” paramedic Will Broughton told Sky News on Tuesday.

Samantha Batt-Rawden, president of the Doctors’ Association UK and an NHS critical care doctor, used Twitter to hit back at those who said health-care workers were exaggerating. “Try holding an iPad for a patient to say goodbye to their family. Or having to . . . ventilate a colleague,” she wrote Monday.

Government figures suggest that the virus is surging in Britain, despite restrictions already in place in most of the country. On Tuesday, 53,135 confirmed cases were reported across Britain, marking the second record day in a row and a number far higher than any single day increase in the first wave.

More widespread testing may account for the new record in confirmed cases, but another number cannot be explained away: NHS England said Monday that a record 20,426 people were being treated for the virus in hospitals in England.

The previous peak number for those hospitalized was set during the first surge in cases in April at a little under 19,000.

Much of Britain, including London, is already under the highest level of lockdown: Tier 4 in the U.K. system. One senior adviser to the government said Tuesday that more of the country should be brought to this level “or higher” to “prevent a catastrophe in January and February.”

“I think we are entering a very dangerous new phase of the pandemic,” Andrew Hayward, an epidemiologist at University College London, told BBC Radio 4.

Health Secretary Matt Hancock is expected to announce any changes to restrictions Wednesday, the BBC reported. Hancock tweeted Tuesday that the pressure on the NHS was now “unprecedented,” and he asked everyone to work to suppress the virus during “these difficult times.”

Earlier this month, officials in Britain voiced concern over the spread of a new variant of the coronavirus that appears to spread more easily. The variant was first identified by British scientists this month, but it has since been found in a variety of countries.

More than 2.3 million cases of covid-19 have been confirmed in Britain since the virus first appeared in the country. More than 70,000 people have died, giving Britain one of the worst death tolls in the world.

Although there have been medical advances in treatment for covid-19, and the British government was the first in the world to begin a widespread immunization program of a fully tested vaccine, the virus appears to be spreading faster than lockdown measures can restrict it.

After almost a full year of fighting the pandemic, the toll is particularly hard on health workers. “This has probably been the toughest year that most of us can remember,” Stevens told reporters.

Simon Walsh, deputy chairman of the British Medical Association’s U.K. Consultants Committee, told the Press Association news agency that hospitals in the worst-hit areas of London were using the same sort of protocols expected in a “major incident.”

“They’re having crisis meetings; they’re calling on staff to come in to work if they’re able to on their days off,” Walsh said.

Health workers quoted in the media suggested that the government has mismanaged its staffing. During the first wave of the virus, the government used empty event spaces to build seven emergency Nightingale hospitals at a cost of 220 million pounds ($297 million).

However, the Daily Telegraph reported that the facilities have remained mostly empty during the new wave of the virus and that some were being dismantled because of shortages in staffing.

Health-care workers also complained that they were not being prioritized for vaccines, which are largely going to the elderly and those with underlying health problems at this stage of the British government’s rollout.

Batt-Rawden wrote Monday that many medical workers are getting sick from the new variant and that some hospitals are tweeting out messages asking for medical students to work in intensive care units.

“This is not a drill. Please believe us,” she tweeted, adding a hands-praying emoji.

The City of London. MUST CREDIT: Bloomberg photo by Jason Alden

The City of London. MUST CREDIT: Bloomberg photo by Jason Alden

Visitors look at an electronic ticker at the Tokyo Stock Exchange on Oct. 29, 2020. MUST CREDIT: Bloomberg photo by Kiyoshi Ota

Visitors look at an electronic ticker at the Tokyo Stock Exchange on Oct. 29, 2020. MUST CREDIT: Bloomberg photo by Kiyoshi Ota