Thailand’s rubber glove industry is aiming to expand its slice of the global market from 15 per cent to 20 per cent in the next five years.

To meet that target, the Thai Rubber Glove Manufacturers Association (TRGMA) is pushing for increased investment and improved overall competitiveness in the industry.

Association president Veerasith Sinchareonkul said the long-term aim was to grab a 40-per-cent share of the world market.

The move follows a 20-per-cent jump in global demand for rubber gloves to 3.6 million amid the Covid-19 pandemic. Demand is expected to rise by another 10 per cent next year.

Veerasith urged the government to provide more financial support to help manufacturers expand investment. It should also streamline regulations to ease the launch of new factories, he added.

Thailand is the world’s second largest exporter of rubber gloves, driven by 19 manufacturers with combined production capacity of 46 billion per year. Of that total, 90 per cent is exported. Medical rubber gloves account for 88 per cent of total production.

“We want to see Thailand become the world’s production hub of natural-rubber gloves,” he said.

China and Malaysia, the world’s major rubber glove makers, have already expanded their production capacity, he added.

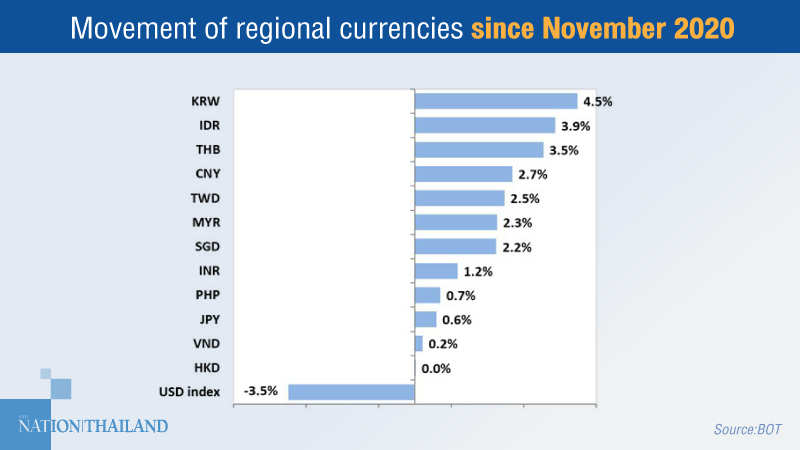

The weakening dollar has seen regional currencies appreciate quickly, with China’s yuan its highest for two and half years, the Korean won and Singaporean dollar strongest in three years, and the new Taiwan dollar at a 23-year high.

Availability of Covid-19 vaccine coupled with signs of global economic recovery in November have caused the US dollar to weaken rapidly, Bank of Thailand (BOT) assistant governor Vachira Arromdee said on Wednesday. The dollar fell to a two-year low against the baht of Bt30.023 on Wednesday, according to BOT figures.Since November, the baht has risen 3.5 per cent, the won 4.5 per cent and Indonesia’s rupiah 3.9 per cent.

Year-to-date, the baht had actually weakened slightly, Vachira noted.

The central bank was closely monitoring currency rates and it would prevent the baht’s value from impacting the economic recovery, she added.

The central bank has introduced a slew of measures to encourage capital outflow in order to balance increasing capital inflows that are driving the baht up.

Thai exporters are complaining that the strong baht makes their products more expensive and less competitive in the global market.

The Siam Commercial Bank’s Economic Intelligence Centre (EIC) expects the Thai gross domestic product (GDP) next year to expand by 3.8 per cent on the back of improving global growth, fiscal stimulus packages and vaccine progress.

Global growth, however, is likely to get worse due to recent Covid-19 resurgences before improving. The recovery in 2021 is likely to be gradual, supported by vaccine progress, stimulus packages and less severe scarring effects.

However, most key economies (except China) in 2021 should remain below their pre-Covid levels in 2019. In late 2020, the Covid-19 resurgences in several countries should result in the tightening of lockdown measures and hence slow economic recovery in the near-term.

Looking forward, global economic recovery in 2021 will likely be gradual and uneven across countries and industries. Developed countries, which are expected to be vaccinated in the first half of the year, should recover faster compared to developing countries.

In Thailand, better-than-expected private consumption recovery in the third quarter of this year should result in smaller-than-expected GDP contraction in 2020.

In the third quarter of this year, Thailand’s GDP fell by -6.4 per cent year on year, supported by faster recovery in private consumption on the back of more holidays and stimulus packages.

However, recovery in the fourth quarter will likely slowdown somewhat due to Covid-19 resurgences in several countries, which should affect consumer confidence and domestic tourism. As a result, EIC expects Thai GDP growth this year to fall by -6.5 per cent versus its previous forecast of -7.8 per cent.

Looking forward, EIC expects the Thai economy next year to grow by 3.8 per cent due to the low base effect, global recovery, fiscal spending and additional stimulus packages as well as Covid-19 vaccine, which is expected to be distributed in the second half of 2021.

However, scarring effects should continue to pressure private domestic demand recovery. Public spending is likely to be a key supportive factor, especially public investment spending.

In addition, the Bt1-trillion recovery package still has about Bt500 billion ready to be disbursed in 2021.

Recently, the government also extended some co-pay measures, suggesting their ready stance to continue fiscal policy easing to support private consumption.

Thai exports in 2021 is expected to rebound and grow by 4.7per cent on the back of global economic and trade recovery. However, the severe shortage and hence rising cost on freight containers in late 2020 and early 2021 as well as strong baht due to weakening dollar should remain key headwinds for export recovery.

The progress in high efficacy rate vaccines, combined with Thailand as a production base for AstraZeneca, should support Thailand’s tourism recovery in the second half of next year, when both key foreign tourists’ countries and Thailand have been widely vaccinated.

On tourist arrival forecasts, EIC expects around 8 million foreign tourists in 2021, which remains significantly lower than the foreign tourist arrivals in 2019 (around 40 million).

Meanwhile, with material scarring effects on Thai economy, the effects should continue to pressure private consumption and investment recovery through:

• Fragile labour markets on the back of elevated unemployment, rising underemployment, and income slowdown,

• Bleak business registration and dissolution expected to continue, and

• Rising household debt to income ratio.

On monetary policy, EIC expects the Bank of Thailand to keep its policy rate at 0.5 per cent throughout 2021.

EIC expects strengthening Thai baht pressure to continue with the baht coming in the range of Bt29.5-Bt30.5 against the dollar at end-2021, mainly due to a weak greenback, resulting from global economic recovery, less volatile global trade tensions, larger US budget deficit, and hence capital inflows to emerging markets, including Thailand.

The key downside risks on the Thai economy in 2021 include Covid-19 resurgences and delay in wide vaccine distribution, and issues on political stability, which could impact investors’ confidence. The other risk is stronger Thai baht, compared with key trading partners, to impact external demand’s recovery.

The Stock Exchange of Thailand (SET) Index closed at 1,482.67 on Wednesday, up 3.75 points or 0.25 per cent. Total transactions amounted to Bt123.39 billion with an index high of 1,503.89 and a low of 1,474.83.

In the morning session, an analyst at Krungsri Securities expected the day’s index to rise to between 1,490 and 1,500 points on the influx of foreign funds in response to positive news of Covid-19 vaccines, adding that the positive sentiment was also benefiting large-cap stocks.

“However, we still advise investors to stick to short-term speculation as the SET will come under pressure from its tight valuation and mass sell-offs to reduce risks during the upcoming long holiday,” he said.

The 10 stocks with the highest trade value today were SAK, KBANK, DELTA, IRPC, ADVANC, PTT, SCB, SCGP, AOT and CPF.

As of 5pm, the price of oil rose by US$0.61 or 1.34 per cent to $46.21 per barrel, while gold dropped by $8.50 or 0.45 per cent, to $1,866.40 per ounce.

Other Asian indices were on the rise, except for Chinese indices:

Japan’s Nikkei Index closed at 26,817.94, up 350.86 points or 1.33 per cent.

China’s Shang Hai SE Composite Index closed at 3,371.96, down 38.21 points or 1.12 per cent, while Shenzhen SE Component Index closed at 13,716.53, down 257.36 points or 1.84 per cent.

Hong Kong’s Hang Seng Index closed at 26,502.84, up 198.28 points or 0.75 per cent.

South Korea’s KOSPI Index closed at 2,755.47, up 54.54 points or 2.02 per cent.

Taiwan’s TAIEX Index closed at 14,390.14, up 29.74 points or 0.21 per cent.

Despite a renewed emphasis on improving relations with traditional allies in Asia, US policy towards China is unlikely to change dramatically under President-elect Joe Biden’s administration, a new report by Moody’s Investors Service published on Wednesday shows.

“We do not expect the Biden administration to result in major changes in Asia credit, with any renewed pivot likely to run up against the reality of longer-term shifts underway that are increasing China’s centrality to the region,” said Nishad Majmudar, a Moody’s assistant vice president and analyst.

With ongoing trade frictions, Biden is unlikely to unwind the actions the Trump administration took against China. And Moody’s expects Biden to embrace recent outreach from the EU on adopting a unified trans-Atlantic approach against China on certain issues, while also searching for areas of cooperation with China’s President Xi Jinping.

“We expect Biden’s multilateral approach towards China will not stop ongoing structural shifts, including the restricting of supply chains and consolidation of the global economy into three distinct blocs, with potential negative credit effects for multinationals and export-oriented companies,” adds Majmudar.

Outside China, Biden’s policy may attempt to revise the “pivot to Asia” adopted by former president Barack Obama, aimed at increasing diplomatic and investment ties with the region.

Biden’s increased engagement in Asia would face a challenge from China’s growing centrality in the region, and could result in countries facing a choice between strengthening security ties with the US or deepening economic ties with China.

Meanwhile, the likely increased focus by the US under Biden on climate policy initiatives will increase longer term credit risks for industrial sectors prominent in many Asian countries, particularly power, automotive, oil and gas, and steel. Similarly, US financial regulators are more likely to follow European efforts pushing for greater financial disclosures of environmental risk, which could create pressure for Asian regulators to follow suit.

Delta Electronics’ share price rose by Bt68, or 20.8 per cent, to Bt395 per share in morning trade on Wednesday, but experts advised against investing in the company’s shares as its price was higher than the base value.

The price of Delta shares had risen more than Bt300 per share since yesterday as the company gained positive sentiment from the sharp rise of its subsidiary’s shares in Taiwan amid positive news of the firm’s Covid-19 test kit.

UOB Kay Hian strategist Kitpon Pripisankit said Delta’s share price went higher than many analysts’ forecast of between Bt200 and Bt250 per share.

“We advise investors to sell some of their Delta shares because its price has already responded to the above-mentioned positive sentiment,” he said.

Meanwhile, Yuanta Securities strategist Natapon Khamthakrue said Delta’s share price had risen higher than its base value and it would be listed on the SET50 Index again.

He added that Delta also gained positive sentiment from hopes over 5G and data centre trends, as well as speculation by Thai institutional investors.

“We advise investors to avoid buying Delta shares as its price would come under pressure from appreciation of the baht. Instead, we advise buying KCE Electronics shares as its price is cheap and is likely to move upside,” he said.

The Stock Exchange of Thailand (SET) Index rose by 22.72 points, or 1.54 per cent, to 1,501.64 in the morning session on Wednesday.

An analyst at Krungsri Securities expected the day’s index to rise to between 1,490 and 1,500 points from foreign fund inflows in response to positive news of a Covid-19 vaccine, adding that this positive sentiment is also benefiting large-cap stocks.

“However, we still advise investors to undertake short-term speculation as the SET would come under pressure from its tight valuation and mass sell-offs of shares to reduce risks during the upcoming long holiday,” he said.

He recommended investors buy:

> Laggard shares in the SET50 Index, such as EGCO, TCAP, DTAC, KTB, TMB, SCB, BCP and TOP.

> MINT, CENTEL and AOT that benefit from positive news of a Covid-19 vaccine.

The SET Index closed at 1,478.92 on Tuesday, up 29.09 points, or 2.01 per cent. Total transactions amounted to Bt123.46 billion, with an index high of 1,484.73 points and a low of 1,442.65.

The price of gold was unchanged in morning trade on Wednesday after surging by Bt300 per baht weight at close on Tuesday, the Gold Traders Association reported.

As of 9.24am, the buying price of a gold bar was Bt26,450 per baht weight and selling price Bt26,550 while gold ornaments cost Bt25,969.08 and Bt27,050, respectively.

The Comex (Commodity Exchange) gold price to be delivered in February next year rose by US$8.90, or 0.48 per cent, closing at $1,874.9 (Bt56,270) per ounce on Tuesday, the highest since November 17.

The gold price gained positive sentiment from hopes of a US Covid-19 relief package and a decline in the US Treasury bond yield.

An analyst at YLG Bullion International advised investors to undertake short-term speculation as mass buy-ups of the precious metal hadn’t increased by much.

“We advise investors to buy gold when the price rises over the line between $1,846 and $1,850 per ounce and take profits if the price cannot rise over the line between $1,878 and $1,887,” he said.

The baht opened at 30.04 to the US dollar on Wednesday, unchanged from the previous day’s close.

The Thai currency is likely to move between 29.95 and 30.15, said Jitipol Puksamatanan, senior director of the chief investment office at SCB Securities.

On Tuesday night, the S&P 500 Index rose by 0.3 per cent amid progress in US financial policy, while the Stoxx 600 Index increased by 0.2 per cent as the ZEW Investor Sentiment Index in December hit 55 points, higher than the market expectation of 46 points.

However, the financial market didn’t open in a risk state as the US ten-year Treasury bond yield was unchanged at 0.91 per cent, while the dollar recovered slightly after positive news of a US economic stimulus package, Jitipol said

Meanwhile, the baht strengthened to near the strongest point of the year – at 30 to the dollar – due to mass sell-offs of the currency by exporters, while some foreign investors have gradually sold bonds to purchase Thai shares for the remainder of the year as they expect the economy to recover, he said.

“We still believe the baht will weaken once the stock market faces a correction,” Jitipol added.

By Syndication Washington Post, Bloomberg · Rita Nazareth, Claire Ballentine

Stocks rose to a record as stimulus talks tempered concern about tougher restrictions amid a surge in coronavirus cases.

The S&P 500 closed at an all-time high after Senate Majority Leader Mitch McConnell, R-Ky., suggested setting aside some issues that have been roadblocks to a relief package — a strategic retreat aimed at striking a deal. The Nasdaq 100 advanced for a 10th straight day, the longest rally in about a year. Pfizer Inc. jumped as U.S. regulators gave early indications they may grant emergency-use authorization to its vaccine. Tesla Inc. erased losses that were driven by plans to raise as much as $5 billion.

Time is running ever shorter on getting fresh stimulus, with lawmakers approaching the year-end break just as U.S. coronavirus infections surpass 15 million. Democrats have opposed McConnell’s insistence on giving employers a shield from lawsuits, while he has been among Republicans blasting Democratic demands for assistance to state and local authorities as a bailout. Both issues have curtailed prospects of an agreement.

“After months of inaction by leaders in Washington, the market is likely to respond well to any movement towards additional fiscal support,” said Adam Phillips, director of portfolio strategy at EP Wealth Advisors. “However, motion is not the same as action. If these discussions do not lead to results, we could see the market give up some of its recent gains.”

A key sentiment indicator for U.S. stocks has reached its most bullish level in two decades. The weekly Cboe ratio of volume traded in puts versus calls fell to the lowest since July 2000 last week. This implies extreme positioning to the upside, as investors look beyond short-term uncertainty toward a continuing global recovery in 2021.

Elsewhere, the pound pared declines after the U.K. dropped controversial parts of an internal bill that would have given it the power to unilaterally override the Brexit divorce treaty. Prime Minister Boris Johnson will hold crisis talks with European Commission President Ursula von der Leyen Wednesday evening as the two sides try to salvage a trade deal by the end of the year.

These are some of the main moves in markets:

Stocks

– The S&P 500 increased 0.3% as of 4 p.m. EST.

– The Stoxx Europe 600 Index climbed 0.2%.

– The MSCI Asia Pacific Index fell 0.1%.

Currencies

– The Bloomberg Dollar Spot Index was little changed.

– The euro was little changed at $1.2106.

– The British pound dipped 0.1% to $1.3366.

– The Japanese yen weakened 0.1% to 104.17 per dollar.

Bonds

– The yield on 10-year Treasuries fell one basis point to 0.91%.

– Germany’s 10-year yield decreased three basis points to -0.61%.

– Britain’s 10-year yield dipped three basis points to 0.257%.

Commodities

– West Texas Intermediate crude fell 0.3% to $45.61 a barrel.