Asset management companies are launching various types of mutual funds in the remainder of this year to meet investors’ needs during market volatility.

SCB Asset Management will this year launch up to six funds worth approximately Bt18 billion – two global equity funds and four complex return funds, said its head of Marketing Strategy and Investment Products Suparat Areewong.

“The global equity fund that focuses on foreign shares will help diversify risks and generate returns in the long term, while the complex return fund will help generate returns in line with the gold price and reduce risks of capital loss,” she said.

Krungthai Asset Management is planning to launch up to six funds worth approximately Bt15 billion this year, including four global fixed income funds and one Retirement Mutual Fund (RMF), said Chatchaphol Srivaleepan, executive vice president of Business Development.

“The global fixed income fund will help generate additional returns and is suitable for customers who can tolerate low and moderate risks, while the RMF focuses on China A-shares and is suitable for long-term investors,” he said, adding that RMF investments are tax deductible.

Kasikorn Asset Management has plans to launch three RMFs worth about Bt15 billion this year.

“The company launched the K-CHANGE-RMF on November 2-6, which focuses on global shares related to green trends, while the K-CHINA-RMF focusing on Chinese shares will be launched soon,” said Navin Intharasombat, first senior vice president for foreign investment management, adding that the K-USA-RMF for US shares is currently awaiting approval.

Tisco Asset Management is launching up to two RMFs worth about Bt2 billion and focused on foreign stock markets that are able to generate better returns than Thai stocks.

“Previously, the company launched four Super Savings Funds that invest in about Bt4 billion of Thai and Chinese shares, and one fund that focuses on stocks related to next-generation internet, such as cloud computing, big data and blockchain,” said Sarat Chatsuwan, director of marketing and investment adviser.

Meanwhile BBL Asset Management will introduce two funds worth about Bt25 billion after launching the Bualuang China A-Shares Equity RMF worth Bt5 billion at the beginning of November.

UOB Asset Management will soon establish two funds, the United China A-Shares Innovation Fund (UCI) and United Sustainable Equity Solution Fund (USUS).

The UCI fund will target China A-shares related to innovation, while the USUS fund will focus on Environmental, Social, and Governance (ESG) stocks.

Online merchants, YouTubers and even social-media influencers may have to start paying income tax after the finance minister announced his ministry targets at least Bt2 trillion in tax earnings from this group.

The Revenue Department plans to collect taxes from at least 500,000 online traders.

The Finance Ministry is also getting ready to propose amendments to the revenue code that cover online sales from overseas in the Senate next week once it collects comments from the House committee.

Ekniti Nitithanprapas, director-general of the Revenue Department, said on Monday that the law will require foreign businesses that use online platforms to provide commercial services in Thailand to register for the payment of value-added tax when their annual income exceeds Bt1.8 million. He said this will put local businesses at a fair footing and will also boost state earnings by at least Bt5 billion.

The Revenue Department will also expand the taxpayers’ base and cover more people, especially those who avoid filing tax returns. Thailand’s taxpayers’ base stands at 9.55 million people, but only 3 million actually pay taxes.

Many people have taken advantage of the Covid-19 crisis by earning extra income from selling products online, developing a YouTube channel or becoming social-media influences, and the ministry is planning to pull at least 500,000 of these people into the tax system next year.

Finance Minister Arkom Termpitthayaphaisit said recently that the Revenue Department should achieve its target of Bt2 trillion for the 2021 fiscal year despite the economic slowdown, as it has developed a new digital system which makes tax collection more efficient.

The Stock Exchange of Thailand (SET) Index rose by 16.51 points, or 1.23 per cent, to 1,362.98 in the morning session on Monday.

An analyst at Krungsri Securities expected the day’s index to rise to between 1,355 and 1,360 points in response to Thailand signing the Regional Comprehensive Economic Partnership (RCEP) agreement and the rise in regional stock indices.

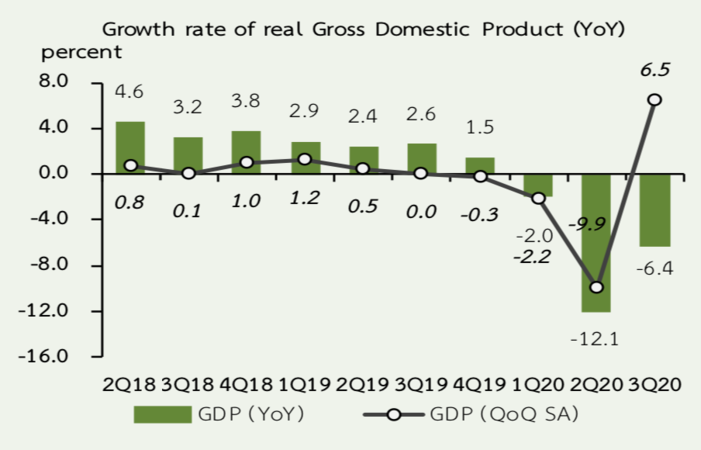

The SET recently gained positive sentiment from the Office of the National Economic and Social Development Council (NESDC) revealing that Thailand’s third-quarter (Q3) gross domestic product (GDP) contracted 6.4 per cent, while the country’s first nine months GDP contracted 6.7 per cent.

The NESDC expected the country’s GDP to contract 6.7 per cent this year and grow 3.5 per cent to 4.5 per cent next year from government disbursement. The baht appreciated to 30.16 against the dollar.

“However, investors should beware of market volatility from uncertainty over the escalating Covid-19 outbreak and domestic political unrest,” he said, adding that pro-democracy protesters will hold an anti-government rally again this week.

He recommended that investors buy:

▪︎ KTC, AMANAH and THANI as Government Savings Bank will conclude partners to work on car registration loans this week.

▪︎ AMATA, WHA, SAT, AH, STGT, STA and RCL that benefit from the RCEP agreement.

The SET Index closed at 1,346.47 on Friday, up 10.16 points or 0.76 per cent. Total transactions amounted to Bt97.02 billion with an index high of 1,352.51 and a low of 1,327.73.

The price of gold rose by Bt150 per baht weight in morning trade on Monday, the Gold Traders Association reported.

As of 9.26am, the buying price of a gold bar was Bt27,000 per baht weight and selling price Bt27,100, while gold ornaments were priced at Bt26,514.84 and Bt27,600, respectively.

At close on Saturday, the buying price of a gold bar was Bt26,850 per baht weight and selling price Bt26,950, while gold ornaments were Bt26,363.24 and Bt27,450, respectively.

Spot gold price moved to US$1,898 (Bt57,211) per ounce in the morning after rising by US$12.9 to $1,886.2 per ounce at close on Friday due to the weakening dollar. However, the metal price in the previous week dropped sharply by 3.24 per cent.

Hong Kong gold price rose by HK$70 to $17,470 (Bt67,918) per tael this morning, the Chinese Gold and Silver Exchange Society reported.

Gross Domestic Product in Q3/2020 decreased by 6.4%, recovering from a fall of 12.1% in Q2/2020, as a result of improvements in total exports of goods and services, private investment, and private final consumption expenditure. Meanwhile, government final consumption expenditure, and public investment both expanded continually, the National Economic and Social Development Council, the state-own think-tank said on Monday.

In terms of production, agricultural production fell by 0.9%, due mainly to the decline in main crops included paddy, rubber, and oil palms. The non-agricultural sector declined by 6.8%, improving from a fall of 12.9% in Q2/2020 as the government has eased the measures to prevent and control the spread of COVID-19. Furthermore, the economic stimulus measures also supported the recovery of manufacturing and service sectors, which fell by 5.3% and 7.3%, improving from falls of 14.6% and 12.2% in Q2/2020, respectively. The recovered service sector included wholesale and retail trade, accommodation and food service activities, and transportation and storage. Moreover, construction and information and communication expanded continually, the NESDC said.

In terms of expenditure, private final consumption expenditure fell by 0.6%. Moreover, gross fixed capital formation, and exports and imports of goods and services contracted by 2.4%, 23.5%, and 20.3%, respectively. However, government final consumption expenditure expanded by 3.4%. After seasonal adjustment, the Thai economy in Q3/2020 expanded by 6.5% (QoQ SA).

Private final consumption expenditure fell by 0.6%, recovering from a fall of 6.8% in Q2/2020. Non-durable and service items expanded by 2.7%, and 3.8%, respectively. However, durable and semi-durable items decreased by 19.3%, and 14.0%, respectively.

General government final consumption expenditure increased by 3.4%, continued to expand from a rise of 1.3% in Q2/2020. The expansion was mainly attributed to compensation of employees, with a 1.6% rise. Moreover, purchases of goods and services grew by 7.8%. In addition, social transfer in kind also expanded by 8.0%.

Gross fixed capital formation fell by 2.4%, compared to a fall of 8.0% in Q2/2020. Private investment decreased by 10.7%, compared to a 15.0% reduction in Q2/2020. Machinery items was a major contributing factor, with a reduction of 14.0%. Meanwhile, construction expanded slightly by 0.3%. Public investment significantly expanded by 18.5%, increasing from a rise of 12.5% in Q2/2020. The expansion was resulted from an 18.4% expansion in public machinery items as well as an 18.6% increase in public construction, driven mainly by the government construction.

Changes in inventories at current market prices in Q3/2020 decreased to the value of 120.6 billion baht. Reduction in stocks came mainly from rice, sugar, motor vehicles, preparation and spinning of textile fibers, and gold. Accumulation in stocks, meanwhile, included rubber, paddy, jewelry and related articles, computers and peripheral equipment, and refined petroleum products.

Goods and services balance at current market prices recorded a surplus of 257.2 billion baht, comprising a surplus of 397.5 billion baht in trade balance and a deficit of 140.3 billion baht in service balance.

The Office of Transport and Public Policy and Planning has hired Infra Plus Consulting for Bt22 million to conduct a study on its plan to build an efficient transport link between the Eastern Economic Corridor (EEC) and the South through Ranong province.

The move is part of the government’s plan to create a transport link between EEC, covering the provinces of Rayong, Chonbur and Chachoengsao, and other parts of the country.

The study should be completed by July next year, the office’s deputy director general Wilairat Sirisoponsilp said.

The plan focuses on upgrading the deep sea port in Ranong and turning it into a trading gateway for the Andaman Sea to accommodate the transfer of goods from EEC to countries that are members of the Bay of Bengal Initiative for Multi-Sectoral Technical and Economic Cooperation (BIMSTEC) as well as to Europe, Middle-East and Africa.

BIMSTEC comprises Bangladesh, Bhutan, India, Nepal, Sri Lanka, Myanmar and Thailand.

NESDC to tap Bt100 billion for funding labour training

EconNov 16. 2020Deputy Prime Minister Supattanapong Punmeechaow

By The Nation

The National Economic and Social Development Council (NESDC) would propose new projects worth Bt100 billion to the Cabinet related to labour skills training and for investments in projects in the communities, council secretary-general Danucha Pichayanan said.

The projects would be funded from the Bt400-billion budget, which is part of the proposed Bt1-trillion borrowing to fund Covid-19 stimulus programmes, added Danucha, who is secreary of the state committee tasked with screening budget requests under the borrowing plan.

The Bt100-billion spending is also in line with Deputy Prime Minister Supattanapong Punmeechaow’s policy to invest Bt400 billion focused on labour upskilling and reskilling.

Meanwhile, Supattanapong has instructed the Eastern Economic Corridor Office and the Board of Investment to seek ways to lure more foreign investment into Thailand.

Earlier, EEC Office secretary-general Kanit Sangsubhan said that the EEC office would adjust its five-year investment plan to adapt to the changing global situation.

The 2020-24 plan for infrastructure and targeted industries would be revised in light of US president-elect Joe Biden’s strategy to promote eco-friendly businesses.

Kanit said the EEC would focus more on trade and investment collaboration with the US, as well as woo foreign investment in new technologies such as 5G wireless broadband.

By The Washington Post · David J. Lynch · NATIONAL, BUSINESS, US-GLOBAL-MARKETS The uncontrolled coronavirus outbreak is prompting government officials across the nation to impose new restrictions on consumers and businesses, sapping the economy’s momentum and delaying the recovery of millions of jobs lost during the recession.

Washington’s failure to provide additional financial support is compounding the economic distress. Though Federal Reserve Chair Jerome Powell this week repeated his call for a fresh round of pump-priming, the economy for now is left to navigate a winter of disease and loss unaided.

On Friday, Virginia Democratic Gov. Ralph Northam tightened limits on restaurants and indoor gatherings, effective at 12:01 a.m. Monday, while the governors of California, Oregon and Washington state issued a joint statement discouraging travel and advising visitors to quarantine upon arrival for 14 days. The mayor of New York City, meanwhile, warned parents that public schools could close as soon as Monday.

Similar measures are taking effect or under consideration elsewhere, including Chicago, where the mayor on Thursday issued a stay-at-home advisory just hours before Illinois Democratic Gov. J.B. Pritzker threatened a mandatory statewide order. The renewed clampdown is reminiscent of the worst days of the pandemic in early March when sports leagues, movie theaters and restaurants abruptly went into hibernation in hopes of curbing the contagion.

Those steps were only partly successful and came at great cost. By the end of June, the economy had shrunk by $2.2 trillion – more than Italy’s entire annual output. Now as communities around the country inch toward new shutdowns, the economy is again at risk. Consumers are growing more pessimistic about the future, according to the latest University of Michigan confidence gauge. And even before new restrictions were announced, they had begun cutting back on spending.

“We see stronger growth in 2021. But we need a bridge to get there,” said economist Gregory Daco of Oxford Economics. “The outlook is honestly quite dark.”

The backsliding comes after a stronger-than-expected rebound from this spring’s abrupt recession. A bit more than half of the 22 million Americans who lost their jobs when nonessential businesses closed have returned to work, and today’s 6.9% unemployment rate is well below the double-digit figures that most Wall Street economists originally had forecast. Output expanded in the third quarter at a record rate.

Yet with more than 11 million still jobless, the United States is in danger of squandering the hard-won progress it has made in rebuilding the economy. On Friday, House Speaker Nancy Pelosi, D-Calif., said the rampaging virus represented “an emergency of the highest magnitude.” But she and Senate Majority Leader Mitch McConnell, R-Ky., have held no talks on a new rescue package.

In El Paso, local officials have deployed 10 mobile morgue trailers to handle a backlog of corpses. The county’s top elected official this week extended a shutdown of nonessential businesses until Dec. 1, ordering residents to stay home and avoid travel.

The pandemic has driven roughly 300 companies out of business in the border community, according to David Jerome, the president of the local chamber of commerce. An additional 300 companies – restaurants, hair salons and retail shops – have only enough cash on hand to survive for less than a month.

“We’re hitting a bit of a tipping point,” Jerome said. “People are getting to the point where they’re pretty stretched. People are vulnerable.”

Eight months into a historic crisis, the United States appears to be suspended in a sort of economic purgatory. The labor market is slowly healing, with initial unemployment claims falling for four straight weeks. But the virus outlook is grim and getting grimmer.

On Thursday, the United States for the first time reported more than 150,000 cases in a single day. Within the next week, the daily total will top 200,000 and is likely to reach 300,000 by early December, according to Ian Shepherdson, chief economist for Pantheon Macroeconomics.

By mid-December, hospitals will be swamped with twice as many coronavirus patients as during the pandemic’s earlier waves “unless most large-population states impose much more severe restrictions on the leisure and hospitality sectors, and on indoor gatherings, very soon,” he wrote in a note to clients Friday.

Consumers already have begun retrenching. Spending by 30 million Chase credit and debit cardholders through Nov. 9 was 7.4 percent below last year’s level and had “fallen notably” over the past two weeks, according to economist Jesse Edgerton of JPMorgan Chase.

Investors are profiting despite the worsening health situation. On Friday, the Dow Jones industrial average rose nearly 400 points and is up more than 11 percent this month. Yet, millions of American households are suffering a silent financial squeeze.

Between the end of September and the end of October, the number of Americans saying it was “very difficult” to pay their usual household expenses rose by more than 2.3 million to 34.8 million, according to the Census Bureau’s pulse survey.

In Los Angeles, Micah Martin, 57, has been struggling to survive since losing his job as a health-care training consultant. He finally received unemployment benefits this summer just as he was preparing to move back to his parents’ home in Oklahoma.

“Since then, it’s been living off fumes,” he said. “I’m aggravated that Nancy Pelosi and McConnell haven’t come up with a compromise. It’s really put a hardship on me and a lot of other people.”

Los Angeles County health officials warned on Friday that tighter activity limits may be imminent if a recent surge in coronavirus cases isn’t contained. The county already is operating under the most restrictive conditions in California’s four-tiered system.

“Covid seems to be out of control here,” Martin said. “I haven’t been to a restaurant since February.”

There are reasons to hope the economy will fare better in the next few months than it did during the pandemic’s first wave. Doctors have more experience treating covid-19, the disease caused by the coronavirus. More Americans are wearing masks and practicing social distancing. And a highly effective vaccine could be widely available by April, according to Anthony Fauci, the nation’s leading infectious-disease specialist.

“The American people’s reaction to the surge will be significantly different from what it was in the spring,” said Michael Strain, an economist with the American Enterprise Institute. “The risk of dying has gone down considerably relative to the spring. People may be willing to take more risks.”

That seems to be true in the resort town of Branson, Mo. Gail Myer, vice president of family-owned Myer Hotels, said the company has kept employees and guests safe through mask-wearing, social distancing and enhanced sanitizing and hygiene.

Though business is down significantly, and he has reduced his workforce by one-third, Myer said October was the company’s best month this year. November could be even better.

“People are tired of not being able to do things they consider normal, and they are also figuring out how to travel comfortably,” Myer said. “I think the economy in the U.S. is getting better and people are figuring out how to make it work for them.”

But the $3 trillion in federal support that cushioned the blow to the economy in the spring is now absent. The resurgent virus may depress activity no matter what government officials do.

“More businesses will be at risk of permanently going out of business, which would dampen labor demand and potentially spur new rounds of layoffs. This suggests the labor market recovery could meaningfully slow or even reverse in coming months as the country tries to get the virus under control,” economists at Bank of America said Friday.

In Chicago, restaurateur Kevin Boehm, 50, closed two of his 20 restaurants and laid off 1,800 of his roughly 2,000 employees in the spring. With the virus spreading uncontrollably, city officials on Oct. 30 reimposed a ban on indoor dining just one month after they had relaxed restaurant capacity limits.

Over a 27-year career, Boehm has had an oven explode in his face and seen a restaurant burn down. But with revenue off by 80 percent, the pandemic has pushed him and his partner in the Boka Group to the brink.

Now, as Boehm contemplates multimillion-dollar financial losses and the prospect of additional layoffs, he is looking to Washington.

“We need Republicans and Democrats to step up and give us the help we need,” he said. “You can only take so many punches.”

The House last month passed legislation to provide $120 billion in grants to independent restaurants amid warnings that 85% of them could fail without assistance. But the Senate has yet to act on the measure.

Ryan Rivett, chief executive of My Place Hotels of America, is also counting on new stimulus legislation. His extended-stay hotel chain remained open throughout the pandemic with managers of some properties sleeping on site to compensate for reduced staffing.

Rivett received a forgivable government loan earlier this year, which was intended to prevent layoffs. But while he can adjust his labor costs as demand fluctuates, his loan payments are less flexible.

“The absence of stimulus is our bigger worry,” he said. “I don’t want to lose our business because we can’t service our debt.

The economic outlook is clouded by the limited nature of some new restrictions. As the escalating health emergency threatens to overwhelm hospital systems, restrictions are spreading to politically conservative states, such as West Virginia, Iowa and Wyoming, that had resisted such measures during earlier phases of the pandemic.

But such efforts remain controversial. In El Paso, Texas Attorney General Ken Paxton is challenging County Judge Ricardo Samaniego’s shutdown order.

In New Germany, Minn., Jean Stelten-Beuning, owner of Top Dog Country Club, an upscale dog-boarding facility, is worried about the next few months.

Last year, at her 35-acre site, complete with a heated canine swimming pool, she boarded 105 dogs over Thanksgiving weekend. Now as officials urge caution about traveling for the holiday, she expects just 35.

She has halved her 28-person staff, as her revenue dropped 55 percent. The state’s daily case total this week reached a new high and the governor ordered new limits on restaurants and other indoor gatherings.

“If the numbers keep growing and these shutdowns keep expanding, I have no idea what’s going to happen,” she said. “It’s going to be pretty bleak.”

Oil falls below $41 with surging covid cases menacing demand

EconNov 14. 2020Storage tanks located near a dock for Hornbeck Offshore Services, Inc. oil industry support vessels in Port Fourchon, La., on June 11, 2020. MUST CREDIT: Bloomberg photo by Luke Sharrett.

By Syndication Washington Post, Bloomberg · Alex Longley · BUSINESS, US-GLOBAL-MARKETS

Oil fell for a second day — dropping below $41 a barrel in New York — as the ongoing spread of coronavirus dampens the demand outlook.

As well as the surge in European coronavirus cases, there are also growing numbers in the U.S., Japan and South Korea, all of which are major oil consumers. The International Energy Agency and the Organization of Petroleum Exporting Countries revised down their demand forecasts this week.

At the same time, supply is rising as Libya opens the taps. The country’s production rose to 1.145 million barrels a day on Friday, according to a spokesman for its state-run National Oil Corp.

Crude is still up more than 8% this week, however, after news of a potential covid-19 vaccine breakthrough spurred a sharp jump in global markets on Monday. Futures have also been supported by indications that the OPEC+ alliance is closing in on a deal to delay a planned easing of output cuts. Still, three of the world’s top central bankers warned that a vaccine wouldn’t be enough to put an end to the economic challenges created by the pandemic as it continues to stymie consumption in some parts.

“There is a clear divergence in the oil demand recovery between Asia and Europe,” said Kevin Solomon, an analyst at brokerage StoneX Group. “We can assume that tighter lockdowns will resume in the United States, ultimately crimping oil demand.”

West Texas Intermediate for December delivery lost 1.9% to $40.35 a barrel as of 1:11 p.m. in London. Brent for January settlement slid 1.4% to $42.93.

In Asia, refiners are having to outbid one another to secure supplies in the spot market as buying interest from Chinese refiners grows. Meanwhile in Europe, where motorway traffic is down by almost 50% in some countries, demand is stuttering anew. That’s impacting crude, with six supertankers of unwanted North Sea oil continuing to float in the region.

Passive oil investors are also taking a more circumspect view on oil in the short term. More than $460 million has been pulled from the market’s largest exchange-traded funds so far this week, according to data compiled by Bloomberg.

U.S. consumer sentiment unexpectedly declines on economic views

EconNov 14. 2020Shoppers walk through the Queens Center shopping mall in the Queens borough of New York on Sept. 9, 2020. MUST CREDIT: Bloomberg photo by Peter Foley.

By Syndication Washington Post, Bloomberg · Jarrell Dillard · BUSINESS, US-GLOBAL-MARKETS, RETAIL U.S. consumer sentiment unexpectedly declined in early November as an increase in covid-19 infections and the election prompted Americans to reassess their outlooks for the economy and finances.

The University of Michigan’s preliminary sentiment index for November decreased to a three-month low of 77 from a final October reading of 81.8, data released Friday showed. The median estimate in Bloomberg’s survey of economists called for a reading of 82.

The measure of expectations dropped by nearly 8 points to 71.3, while a gauge of current conditions was little changed at 85.8. Interviews conducted following the election recorded a substantial negative shift in Republicans’ expectations and no gain among Democrats. The survey began Oct. 28 and concluded late on Nov. 10.

“Republicans now voice the least favorable economic expectations since Trump took office, and Democrats have voiced more positive expectations,” Richard Curtin, director of the survey, said in the report. “In the months ahead, the partisan gap is likely to enlarge, although the gains will be limited until a potential vaccine is approved and widely distributed.”

Consumers’ views about their current financial situations deteriorated, to well below the pre-pandemic peaks, the report showed. Net declines in household incomes were reported in early November for the first time since March 2014, with the largest decrease among lower income households and older Americans.

Less optimism about the state of the economy may damp prospects for the holiday shopping season against a backdrop of surging new virus infections across the country. The rising caseloads could weigh on sentiment in the coming months as some cities and states reinstate more restrictive measures.

A separate report on Thursday showed that the modest momentum in the labor market’s recovery remains intact, with initial jobless claims falling by the most in five weeks.

Deputy Prime Minister Supattanapong Punmeechaow

Deputy Prime Minister Supattanapong Punmeechaow  Federal Reserve Chair Jerome Powell

Federal Reserve Chair Jerome Powell  Storage tanks located near a dock for Hornbeck Offshore Services, Inc. oil industry support vessels in Port Fourchon, La., on June 11, 2020. MUST CREDIT: Bloomberg photo by Luke Sharrett.

Storage tanks located near a dock for Hornbeck Offshore Services, Inc. oil industry support vessels in Port Fourchon, La., on June 11, 2020. MUST CREDIT: Bloomberg photo by Luke Sharrett.  Shoppers walk through the Queens Center shopping mall in the Queens borough of New York on Sept. 9, 2020. MUST CREDIT: Bloomberg photo by Peter Foley.

Shoppers walk through the Queens Center shopping mall in the Queens borough of New York on Sept. 9, 2020. MUST CREDIT: Bloomberg photo by Peter Foley.