#SootinClaimon.Com : ขอบคุณแหล่งข้อมูล : หนังสือพิมพ์ The Nation.

America’s biggest companies are flourishing during the pandemic and putting thousands of people out of work

InternationalDec 17. 2020 Gary Walker was laid off from Salesforce in August after 12 years with the company. MUST CREDIT: Washington Post photo by Jahi Chikwendiu

Gary Walker was laid off from Salesforce in August after 12 years with the company. MUST CREDIT: Washington Post photo by Jahi Chikwendiu

By The Washington Post · Douglas MacMillan, Jonathan O’Connell, Peter Whoriskey, Chris Alcantara

As the coronavirus pandemic devastated small businesses and plunged millions of Americans into poverty this summer and fall, executives at some of the country’s largest corporations sounded surprisingly upbeat.

Restaurant owner David Mainelli stands in front of the former location of his family’s restaurant, Julio’s, in Omaha, Neb., earlier this month. The restaurant group has been a staple in the community since 1977, and announced they were closing their doors in June 2020. MUST CREDIT: Washington Post photo by Carley Scott Fields

“I don’t think we’ve ever been more excited or energized about our prospects,” PayPal finance chief John Rainey said on a November conference call.

“These are times when the strong can get stronger,” Nike chief John Donahoe told analysts in September.

“With all that’s happening around the world, it’s really unfortunate,” said Jensen Huang, chief executive of graphics chip maker Nvidia, during an August earnings call. “But it’s made gaming the largest entertainment medium in the world.”

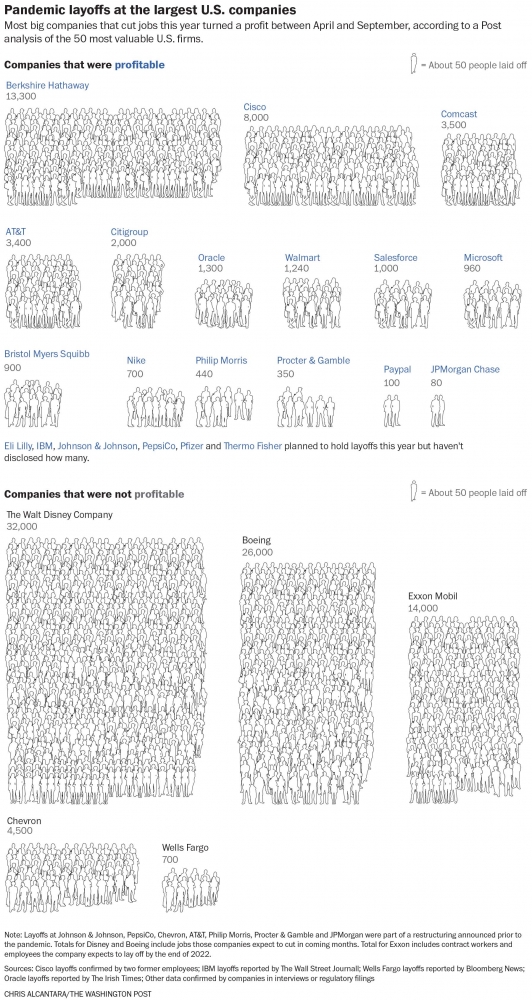

With few exceptions, big businesses are having a very different year from most of the country. Between April and September, one of the most tumultuous economic stretches in modern history, 45 of the 50 most valuable publicly traded U.S. companies turned a profit, a Washington Post analysis found.

Despite their success, at least 27 of the 50 largest firms held layoffs this year, collectively cutting more than 100,000 workers, The Post found.

The data reveals a split screen inside many big companies this year. On one side, corporate leaders are touting their success and casting themselves as leaders on the road to economic recovery. On the other, many of their firms have put Americans out of work and used their profits to increase the wealth of shareholders.

When the coronavirus struck, big companies promised to help battle the crisis. Dozens of prominent chief executives, who last year signed a public pledge to focus less on shareholders and more on the well-being of their employees and broader communities, appeared eager to make good on that promise. Many suspended payments to investors and vowed not to hold layoffs.

Then, 21 big firms that were profitable during the pandemic laid off workers anyway. Berkshire Hathaway raked in profits of $56 billion during the first six months of the pandemic while one of its subsidiary companies laid off more than 13,000 workers. Salesforce, Cisco Systems and PayPal cut staff even after their chief executives vowed not to do so.

Companies sent thousands of employees packing while sending billions of dollars to shareholders. Walmart, whose CEO spent the past year championing the idea that businesses “should not just serve shareholders,” nonetheless distributed more than $10 billion to its investors during the pandemic while laying off 1,200 corporate office employees.

Kirk Hanson, an author and longtime professor of business ethics, says it’s incumbent upon America’s top corporations to help pull the country through the worst recession in decades, particularly given the outsized profits they’re enjoying.

“There is an obligation on the part of the largest and most successful businesses to help buffer the human impact of the crisis,” said Hanson, now a senior fellow at Santa Clara University’s Markkula Center for Applied Ethics.

Instead, Hanson said, they have contributed to the country’s growing economic divide.

The Post contacted all 27 large firms that held layoffs this year. Many said the cuts were not related to the pandemic, but rather, a necessary part of broader “restructuring” plans, where companies shift spending from declining lines of business to growing ones. In some cases, these plans were decided before the pandemic.

Several emphasized that they hired more people this year than they let go. Anne Hatfield, a spokeswoman for Walmart, said everyone the retailer laid off during the pandemic was offered another job in the company, though she declined to say whether the new roles held the same level of pay and responsibilities as the jobs that were eliminated.

Others pointed to the work they have done to help ease the pain in their communities, such as expanding health and family benefits to employees and distributing personal protective equipment to front-line workers. Cisco gave $53 million in cash and PPE to vulnerable populations and PayPal pledged $530 million in investments in minority-owned small businesses.

In an email, Berkshire Hathaway chief executive Warren Buffett said he leaves all decisions at his subsidiary companies to the management of those companies. Airplane parts maker Precision Castparts, which Berkshire Hathaway acquired in 2015, was forced to cut staff due to a severe drop in demand for new planes, he said. Buffett added that he has given $2.9 billion of his personal wealth to charitable causes this year.

The majority of America’s largest corporations have prospered in the coronavirus economy.

Millions of consumers spent more time and money online during government-mandated lockdowns, watching Netflix, viewing ads on Google and Facebook pages, filling Amazon shopping carts and turning the video game business into a bonanza for Nvidia, Microsoft and others. (Amazon founder Jeff Bezos owns The Washington Post.)

Shoppers began splurging on cleaning supplies, hobbies, home cooking and home improvements, driving record growth at big-box stores including Home Depot and Walmart.

Even in the hardest-hit sectors, such as restaurants, travel and hospitality, the biggest companies were largely insulated from the worst of the virus’s reckoning. While independent restaurants struggled to survive, McDonald’s ramped up its takeout and drive-through operations, rolling out new apps and technology catering to on-the-go orders.

In many industries, the giants devoured market share ceded by small businesses, who lacked the resources to keep stores open during unpredictable swings in customer demand. While the 50 largest companies averaged 2% revenue growth over the first nine months of 2020, small business revenue shrank 12% over the same period, according to data collected by software provider Womply from thousands of small firms.

Economists estimate at least 100,000 small businesses permanently closed in the first two months of the pandemic alone.

“Once you kill competition, it’s always hard to restore it,” said Matt Stoller, director of research at the left-leaning American Economic Liberties Project. “This is an extinction-level event for small businesses.”

As the pandemic wore on, many companies kept their promises not to lay off staff. Others saw the recession as a good excuse for trimming labor costs.

In April, cigarette maker Philip Morris made a public commitment to forgo layoffs during the pandemic to help support the “job security and peace of mind” of its 73,000 workers.

“The company will not terminate the employment of any [Philip Morris] employee during this crisis period, unless for cause, and the company has also put on hold any restructuring plan,” Philip Morris said in a news release.

But in June, as infection rates continued to rise, Philip Morris said in a regulatory filing it would eliminate up to 440 workers in New York and Switzerland as part of a restructuring.

In a statement, Philip Morris spokesman Sam Dashiell said the company resumed the restructuring at its Swiss operations center because it determined “prolonging it further would be unfair to everyone.” He declined to explain why the New York layoffs resumed.

Current and former employees at some of these companies say they weren’t surprised to see their leaders renege on promises to retain staff through the pandemic. They didn’t put too much faith in those promises in the first place.

“The choices that they make are governed by, essentially, maximizing shareholder value,” said Gary Walker, a systems engineer who was one of 1,000 employees Salesforce cut in late August.

At the onset of the pandemic, Chuck Robbins described the need to keep workers employed as a moral imperative. The chief executive of Cisco, a $180 billion software and networking giant, said large companies like his shouldn’t lay off workers during a global crisis because, even in a bad year, they had the resources to maintain payrolls.

“Why would we contribute to the problem?” Robbins asked in an interview with Bloomberg News published in April. “To me, it’s just silly for those of us who have the financial wherewithal to absorb this, for us to add to the problem.”

Four months later, Cisco began implementing a plan to lay off at least 8,000 employees, according to two former employees briefed on the plan – the largest round of job cuts the San Jose, Calif.-based company has seen in years.

The majority of Americans who lost jobs this year were laid off from small businesses, many of which had no option but to cut workers to stave off financial collapse.

But larger companies actually laid off a greater portion of their workforces over that period – 9% for large firms versus 7% for smaller firms – despite having more resources to survive the downturn. Their layoffs were quietly acknowledged in regulatory filings and shrouded in corporate jargon, like an “involuntary reduction of associates” at Coca-Cola; and “operating model changes to streamline and speed up strategic execution” at Nike.

The Salesforce layoffs punctuated one of the software giant’s fastest periods of growth and followed frequent pledges by its chief executive to assist with coronavirus relief. Marc Benioff, a self-styled leader of the corporate philanthropy movement, said in a series of tweets in late March that Salesforce pledged “not to conduct any significant lay offs over the next 90 days.”

He suggested all CEOs should take a similar “90 day pledge” and encouraged all Salesforce employees to keep supporting hourly workers, such as housekeepers and dog walkers, who do work for them.

Making good on that pledge was not hard for Salesforce, a company sitting on more than $9 billion in cash and short-term investments. It generated $2.7 billion in profit during the first six months of the pandemic, as businesses flocked to Salesforce’s tools for helping them manage operations remotely.

The layoffs, about five months after Benioff’s tweet, were part of a plan to “reallocate resources” including “eliminating some positions that no longer map to our business priorities,” the company said in a statement. They were announced one day after the software giant announced its biggest quarter of profit and revenue in history, sending its stock soaring 30%.

“Of course I’m cheesed about it. How could you not be?” said Walker, who was laid off after 12 years at the company. “It’s not great timing.”

Walker, 48, who lives with his wife and two dogs in Herndon, Va., said he appreciates Salesforce giving him generous severance benefits and understands large companies sometimes have to cut labor costs to please investors.

Cheryl Sanclemente, a Salesforce spokeswoman, said in a statement the company offered to help all of the people who were affected find new jobs, including in some 12,000 openings it expects to fill over the next year. She added that the company has provided protective equipment to health-care workers throughout the pandemic and gave $30 million to organizations fighting the covid-19 crisis.

Salesforce declined to make Benioff available for an interview but pointed out that the company did make good on his promise not to hold layoffs within 90 days of his tweet.

Similarly, Wells Fargo explained that it never committed to a time frame when it pledged to pause layoffs – which the company referred to in a statement as “job displacements” – back in March.

“At that time, we said we would continue to evaluate and did not pledge to pause job displacements for a specific period of time,” spokeswoman Beth Richek said in an email. “Starting in early August, we resumed regular job displacement activity.”

She declined to comment on the number of workers who were affected, though sources told Bloomberg News the San Francisco-based bank was cutting the first 700 workers in what is expected to be a massive restructuring impacting tens of thousands of jobs over the coming years.

Then there’s Cisco, which started the year determined not to “add to the problem” of pandemic unemployment, in the words of its CEO. Despite benefiting from a quarantine-fueled boom in videoconferencing tools including its Webex software, the company lost ground to Zoom and reported slowing growth in its cloud computing business.

Robbins, who spent the first few months of the pandemic repeatedly reassuring staff that their jobs would be safe, by summer acknowledged a round of cost-cutting was needed, according to three former employees who were in meetings with Robbins this year and left the company within the past three months. The former employees – two who left voluntarily, one who was laid off – all spoke on the condition of anonymity while discussing their former employer.

Cisco began a restructuring plan to eliminate $1 billion in costs, including a campaign to ask employees to take voluntary retirement packages or a 20% pay cut in exchange for working four days a week, the people said. In addition to the voluntary departures, Cisco began conducting involuntary layoffs in the early fall with the goal of trimming at least 8,000 employees, or more than 10% of its workforce, said two of the former employees who heard this number directly from Cisco managers involved in the plan.

Jennifer Yamamoto, a Cisco spokeswoman, said the company is increasing its investments in certain business areas and reducing investments in others. She declined to specify the number of people Cisco laid off but said 8,000 was not accurate. Cisco was supporting employees who were transitioning out of the company, she said.

Asked about Robbins’s statements from earlier this year, Yamamoto said the CEO “did not commit to no layoffs, but rather said we would preserve what we could depending on how the pandemic played out, and he would then assess the needs of the business every 60 days before making any decisions. As the pandemic continued, things changed in the macro landscape and we had to make some tough choices.”

Nowhere has the disparity between big and small businesses ballooned during the pandemic the way it has for restaurants. Just ask Dave Mainelli.

For more than two decades Mainelli and his family have owned and run Julio’s Restaurant, a Tex-Mex joint in Omaha, Neb. His wife headed operations, his brother was a manager, and his son, a bartender. Customers held birthday parties and family reunions, plus wedding and funeral receptions there.

When the pandemic hit and business started to falter, Mainelli said he tried to keep Julio’s open because of the difficulty of telling many of his longtime employees that it was over. He cut back on hours and eventually on staff, dropping from 40 to a dozen as he tried to survive on delivery and pickup.

But with thin margins and debts beginning to mount, he closed Julio’s for good in June, after 25 years in business.

“There were a lot of tears. It was one of the hardest things I’ve ever been through and I’ve been through a lot of hard stuff,” he said.

While one in six restaurants permanently closed during the first months of the pandemic, according to the National Restaurant Association, big chains have ramped up their drive-through operations and rolled out new apps and menus catering to on-the-go orders.

Maybe no one has done this better than McDonald’s, which was battered by the pandemic in the spring but has since been gobbling up more business by the day, using its scale to outpace hundreds of thousands of competing restaurants.

Analysts say McDonald’s has leveraged its advantages by quickly simplifying its menu, allowing its locations to serve more customers in a shorter time without them having to enter its restaurants. Deliveries and mobile app use is growing. Drive-through orders grew to account for 90% of McDonald’s sales during the pandemic, up from two-thirds of sales before this year.

“The large companies have these asset bases that the smaller companies cannot compete with, particularly now,” said Lauren Silberman, an analyst at Credit Suisse.

Contrast that with the options available to Mainelli. To boost delivery sales he partnered with a local service in Nebraska, but it cut into profits dramatically. “When you rely on delivery, your margins get shrunk because you’re paying them a chunk,” he said.

McDonald’s and other chains have long focused on data analysis and app development, capabilities they are now employing during the pandemic. Its digital drive-through menus allow restaurants to customize menu items for factors such as time of day, the weather and current restaurant traffic.

It is also testing tools for tailoring menus more specifically to customers as they arrive. So, if you have been ordering a Big Mac meal with fries and a large Sprite since the beginning of the pandemic, McDonald’s could begin identifying you through the app running on your phone and start displaying that meal more prominently when you pull up to the drive-through.

Not every McDonald’s franchise has flourished. But for those facing a cash crunch, the company put up nearly $1 billion to allow franchise owners to defer rent and royalty payments until their business returned, a luxury few other restaurant owners enjoy. “Because of our scale and financial stability, we were able to quickly provide franchisees with financial support when they needed it most,” Kevin Ozan, McDonald’s chief financial officer, told investors in November. Company spokespeople declined to comment further.

The result for McDonald’s shareholders has been a gift better than the plastic toy at the bottom of any Happy Meal. In October, shares of its stock reached an all-time high – up 27% since the beginning of March – and the company increased its dividend 3%.

The gulf between McDonald’s and most independent restaurants is staggering. Restaurant employment is down 17% during the pandemic, according to the Independent Restaurant Coalition, with more than 2 million restaurant workers out of a job heading into winter. Many of the owners that are permitted to remain open are doing so by slashing staff and costs and focusing on takeout as much as possible.

At Kayla’s Kitchen and Closet, located in tiny Park Falls, Wis., the menu offers soups, salads and a spicy blackberry bacon panini. Owner Kayla Myers also operates a clothing store next door offering Levi’s jeans, Minnetonka moccasins, children’s clothing and tuxedo rentals.

She said she has been boosting sales with Facebook posts. But she closed off half of her six tables for social distancing measures and cut hours. “You don’t have any point in opening if people can’t even come in,” she said.

After closing Julio’s this year, Mainelli sold the brand and became a writing instructor at local colleges. He and his wife gawk at the long lines of cars at McDonald’s, and he predicts the same fate for independent restaurants that locally owned bookstores faced when Amazon first arrived.

“The same thing is going to happen to the restaurants,” he said. “It’s going to be Olive Garden, Applebee’s and Chili’s. There are not going to be any independents.”

– – –

When Apple announced its quarterly earnings in the spring, chief executive Tim Cook eagerly shared all the company was doing to combat the coronavirus, from manufacturing and distributing face shields to donating $15 million to relief efforts in the earliest days of the pandemic.

But those investments stood in stark contrast to the $50 billion Apple said it planned to spend on stock repurchases – an amount so closely watched by Wall Street that one analyst asked why it appeared slightly lower than previous years.

“The $50 billion share repurchase authorization is impressive enough in absolute terms, but it is a bit lower than the last couple of years,” Katy Huberty, a managing director at Morgan Stanley said during the April conference call. “Any context around the thought process of landing on $50 billion?”

The world’s largest companies have set extraordinary expectations for their annual cash payments to investors. After pausing dividends and share buybacks in the spring, many companies resumed investor payouts by the summer.

The top 50 firms collectively distributed more than $240 billion to shareholders through buybacks and dividends between April and September, representing about 79% of their total profits generated in that period. Except for the five companies that didn’t offer buybacks or dividends this year, no large firm came anywhere close to spending as much on coronavirus relief efforts as they did paying out investors.

Companies often buy their own stock during difficult economic periods to signal to the market that management still believes in their prospects. But those buybacks also mean companies are taking money that could have been invested into employees and innovation and giving it to shareholders, who tend to be high-income individuals and families.

“This is a global crisis but the big companies are not treating it as one – they haven’t skipped a beat,” said William Lazonick, an emeritus economics professor at the University of Massachusetts at Lowell. “Apple gave back tens of billions of dollars to shareholders,” he added. “It’s sick.”

Apple spent $41 billion buying shares and paying cash dividends between April and September, more than twice as much as the company with the next highest total, Microsoft. The tech giants top the list partly because they have come under pressure from shareholders to return some of their enormous stockpiles of cash.

Apple spokesman Josh Rosenstock said supporting worldwide covid-19 relief efforts has been the company’s top priority. Apple has donated “hundreds of millions of dollars” to supporting communities this year including distributing 30 million face masks and 10 million face shields, he said.

The computer maker also kept paying retail employees while its stores were closed, Rosenstock added, and is “working with our suppliers to ensure their staff, including janitors and shuttle drivers, are being paid as well.”

Giant companies across all sectors have raised their dividends and buybacks since 2017, when tax legislation championed by President Donald Trump and passed by Congress lowered the statutory corporate tax rate from 35% to 21%. As a result, many companies explicitly said they would spend some of their tax savings on higher payments to shareholders.

Pharmaceutical giant AbbVie achieved the lowest effective tax rate among all 50 largest firms, paying just 6.5% last year by structuring its business to take advantage of overseas tax havens, the company said in filings. According to Reuters, AbbVie holds dozens of patents for its best-selling rheumatoid arthritis drug Humira in Bermuda, which has no corporate income tax.

Shortly after the tax law was passed, AbbVie chief executive Richard Gonzalez said the company’s cash flow “far exceeds what we are able to use productively to support the business” and therefore would give larger sums to shareholders. This year, he delivered: AbbVie paid investors $4 billion during the first six months of the pandemic, more than twice the amount of profit the company generated in that period.

AbbVie did not appear to lay off any employees this year. The company did not respond to multiple requests for comment.

The Marriner S. Eccles Federal Reserve building. Photographer: Stefani Reynolds/Bloomberg

The Marriner S. Eccles Federal Reserve building. Photographer: Stefani Reynolds/Bloomberg  The Federal Reserve Board building on Constitution Avenue in D.C. (Brendan Mcdermid/ Reuters)

The Federal Reserve Board building on Constitution Avenue in D.C. (Brendan Mcdermid/ Reuters)  Customers wearing protective masks shop during the festival of Dhanteras at the Lajpat Nagar market in New Delhi on Nov.13, 2020. According to Oxfam, nine out of 10 people in underdeveloped countries will miss out on a vaccine in 2021. MUST CREDIT: Bloomberg photo by Prashanth Vishwanthan.

Customers wearing protective masks shop during the festival of Dhanteras at the Lajpat Nagar market in New Delhi on Nov.13, 2020. According to Oxfam, nine out of 10 people in underdeveloped countries will miss out on a vaccine in 2021. MUST CREDIT: Bloomberg photo by Prashanth Vishwanthan.

The Marriner S. Eccles Federal Reserve building in Washington, D.C., on Aug. 18, 2020. MUST CREDIT: Bloomberg photo by Erin Scott.

The Marriner S. Eccles Federal Reserve building in Washington, D.C., on Aug. 18, 2020. MUST CREDIT: Bloomberg photo by Erin Scott.  Recep Tayyip Erdogan, president of Turkey, in Brussels on March 9, 2020. MUST CREDIT: Bloomberg photo by Geert Vanden Wijngaert (Bloomberg).

Recep Tayyip Erdogan, president of Turkey, in Brussels on March 9, 2020. MUST CREDIT: Bloomberg photo by Geert Vanden Wijngaert (Bloomberg).  A pedestrian passes an available retail space in Chicago on May 7, 2020. MUST CREDIT: Bloomberg photo by Christopher Dilts.

A pedestrian passes an available retail space in Chicago on May 7, 2020. MUST CREDIT: Bloomberg photo by Christopher Dilts.  German Chancellor Angela Merkel in the Bundestag in Berlin, on Dec. 16., 2020. MUST CREDIT: Bloomberg photo by Rolf Schulten.

German Chancellor Angela Merkel in the Bundestag in Berlin, on Dec. 16., 2020. MUST CREDIT: Bloomberg photo by Rolf Schulten.  A health care worker receives the Pfizer-BioNTech Covid-19 vaccine in San Diego on Dec. 15, 2020. MUST CREDIT: Bloomberg photo by Bing Guan.

A health care worker receives the Pfizer-BioNTech Covid-19 vaccine in San Diego on Dec. 15, 2020. MUST CREDIT: Bloomberg photo by Bing Guan.