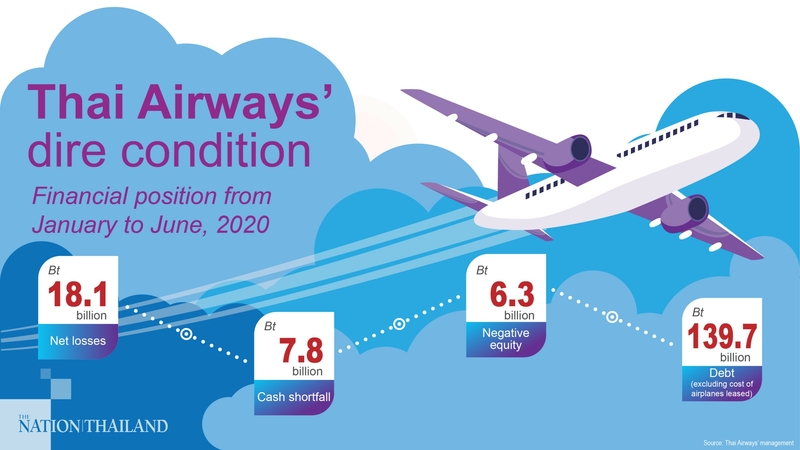

#ศาสตร์เกษตรดินปุ๋ย : ขอบคุณแหล่งข้อมูล : หนังสือพิมพ์ The Nation.

Emergency payroll loans totaling $221 million have gone to at least 21 publicly traded energy companies, and a survey of those companies’ finances shows just how volatile and troubled that sector of the economy has been.

The federal loan program is limited to smaller businesses – firms that in the energy field have been the most vulnerable to the downdrafts that even before the pandemic were running counter to the general growth in the national economy.

Several of the firms were in serious financial straits; for them, the loans are at least a temporary lifeline, but not a solution to their problems. They come against the head winds of sharp stock declines, millions of dollars in losses over the past year, and large global surpluses of oil, coal and gas.

Lenders wouldn’t normally do business with companies that may be on the road to bankruptcy. But the emergency loan effort – called the Paycheck Protection Program – is different.

Its purpose is to pump money into the economy, keeping employees on the payroll and making it possible for businesses to pay their bills and survive what was expected to be a relatively short-term period of revenue loss, said Ann Marie Mehlum, an Obama-era official of the Small Business Administration, which is administering the loans. A PPP loan, according to the sponsors of the Cares Act, which created the program, is essentially supposed to be a grant, extended with the expectation that it will be forgiven.

One recipient – a coal mining company called Rhino Resource Partners, of Lexington, Kentucky – informed the Securities and Exchange Commission in its annual report for 2019 that it might not be able to survive to the end of 2020. Its share price has cratered and its losses mounted. On April 29, it received a maximum $10 million emergency loan thanks to the PPP effort.

A few other companies, on the other hand, have received loans even while business seems to be looking up.

Most striking in that group is Gulf Island Fabrication, of Houston, which received a $10 million PPP loan as it was also closing on a $129 million Navy contract to build two towing, salvage and rescue vessels.

The company did not respond to requests for comment.

“In this challenging and uncertain time, the PPP Loan proceeds provide necessary liquidity to defray payroll and benefit costs, including maximizing our ability to retain our workforce, execute our current backlog and compete for new project awards,” Gulf Island’s CEO, Richard Heo, was quoted as saying in a company news release. “We have already used a portion of the borrowed funds to return a number of employees we had furloughed at the onset of the pandemic and we have retained additional employees we would have had to furlough or terminate without such funds.”

For the first three months of this year, as the pandemic was setting in, the company reported $5.9 million in income on $78.6 million in revenue.

And UR-Energy, a uranium company based in Littleton, Colo., was awarded an $893,000 loan though the spot price of uranium has jumped 30%, imports are down, and demand is steady. Its workforce remains “healthy and fully employed,” the company said.

The loan comes as the Trump administration has been moving to shore up the domestic uranium industry.

The purpose of the PPP loans is to support two months’ worth of employment amid the coronavirus pandemic. If companies spend at least 75% of the loan money on wages and benefits, and the rest on ordinary overhead charges, up to 100% of the loan will be forgiven. Guidance by the Treasury Department cautions that recipients have to show that the loan is necessary to continue operations, and that there aren’t available alternatives.

Companies have until the end of the day Monday to return loans if they decide they can’t meet that standard. One energy firm, Dawson Geophysical, of Midland, Texas, announced that it will repay the $6.4 million loan it received in April.

UR-Energy said in a filing with the Securities and Exchange Commission that “we believe we will be able to meet the [loan] program requirements.”

Most of the other energy companies surveyed by The Washington Post have considerably weaker prospects, and would struggle to secure additional credit, as investors have largely turned away from the sector.

The PPP program, as a result, has put the federal government in the position of funneling money into companies with decidedly problematic balance sheets. And all but one of the 21 companies surveyed received considerably more than the average loan for all sectors, which in the first round in April was $206,000. Eleven firms received more than $5 million, which puts them in the top quarter of 1 percent of all loans.

Two companies – ENGlobal Corporation, of Houston, and Profire Energy, of Lindon, Utah – have been informed that their stock price has fallen so low that they are set to be delisted by the Nasdaq exchange. Amplify Energy, of Houston, has been similarly notified by the New York Stock Exchange.

Profire, an oil field technology company, got a $1.1 million loan. ENGlobal, an engineering services firm that warned at the end of 2019 that it has no access to credit, received $4.9 million. Amplify, an oil and gas producer that has seen its stock drop 88% in the past 52 weeks, got $5.5 million. It lost $35 million last year on revenue of $276 million, even as it was spending $26 million in a stock buyback.

Another energy company that bought back its own stock last year, Independence Contract and Drilling, of Houston, nonetheless saw its share price decline 80% leading up to the onset of the pandemic. It received a $10 million PPP loan.

Rhino Resource Partners, the company that had warned it might not be able to stay in business, operates coal mines in Appalachia, Illinois and Utah, and it has been hammered by the low price of competing natural gas and the sharp falloff in demand for coal. Between its high point in 2019 and Feb. 13, when the stock market started to crash, the share price for the firm had already dropped by 65%.

“The firm was in terrible financial shape before the collapse of coal demand and gas prices; the current pricing environment only exacerbates that issue,” Anthony Campagna, global director of fundamental research at ISS EVA, a corporate analytics firm, wrote in an email. “The firm has not sustainably earned above its cost of capital (creating economic value) in nearly a decade.”

Until 2014, it was run by David Zatezalo, now the assistant secretary of labor in charge of the Mine Safety and Health Administration. His office said he has no current connection to the company, and did not take part in any conversations or correspondence concerning the PPP loan.

In a follow-up phone call, Campagna said, “They’re getting hit from all angles. Hemorrhaging cash. It’s not pretty.”

The company reported losing $100 million last year on $181 million in revenue.

Rhino lists employment at 605 workers, but it has idled at least some of its mines. (The standard limit for receiving an SBA loan is 500 employees, but mining companies and some other firms can go above that.)

The company was assessed fines of $411,000 last year for safety violations. Most – 191 – were for “alleged violations of health or safety standards that could significantly and substantially contribute to a serious injury if left unabated.” Two were for more serious threats to safety and one was for delaying the abatement of a violation. The mine that was cited most often, the Riveredge Mine in Calhoun, Kentucky, was abandoned in November, Laura McGinnis, spokeswoman for the Mine Safety and Health Administration, wrote in an email.

Violations at other company mines continued this spring, even as Rhino was applying for the loan. At its Hopedale mine in Ohio, where 125 miners are employed, repeated inspections spurred by higher-than-normal methane leakages turned up 41 violations through the end of April, according to records of the Mine Safety and Health Administration.

Numerous requests for comment from Rhino have gone unanswered.

Campagna notes that the point of the PPP loans is “not to pick winners and hurt losers,” but to keep workers employed.

Could Rhino have received an ordinary $10 million loan? “Absolutely not,” he said.

“SBA is following the law as it executes the PPP program as defined by the CARES Act passed by Congress,” wrote Carol Wilkerson, a spokeswoman for the Small Business Administration, in an email, in response to a question as to the advisability of lending money to a company in as much difficulty as Rhino.

Another coal company, Indiana-based Hallador, saw its stock price drop by 79% before the pandemic hit. The company hired former EPA administrator Scott Pruitt as a lobbyist last year. It, too, received a maximum $10 million PPP loan.

Of the 21 companies surveyed, one has seen its stock price go up over the past year: EVO Transportation and Energy Services, of Peoria, Arizona, which has a contract with the U.S. Postal Service to haul mail in trucks with alternative fuels. It received a $10 million loan.

The other 20 firms saw their stock prices decline by an average of 47% from last year’s high to the eve of the pandemic crash. During that same period, ending Feb. 23, the Dow Jones average climbed nearly 20%.

When the current PPP loans have run their eight-week course, sometime in June or early July, those companies will at best have postponed their financial problems – and the economy overall promises to be less healthy than it was before the virus hit.

“We have a history of operating losses and have used significant amounts of cash for operations and to fund our acquisitions and investments,” Acorn Energy, of Wilmington, Delaware, which owns electric power plants, declared in an SEC filing. “The market price of our common stock has fluctuated substantially in the past and is likely to continue to be highly volatile and subject to wide fluctuations. During 2019, our common stock traded at prices as low as $0.20 and as high as $0.45 per share.”

Acorn received a $461,000 loan.

Capstone Turbine, of Van Nuys, California, has never made an annual profit since its founding in 1988, running up a deficit of $879 million over the years. It got a $2.6 million loan.