The price of gold rose by Bt300 per baht weight (15 grams) in morning trade on Friday (August 14), the Gold Traders Association reported.

As of 9.23am, the buying price of a gold bar was Bt28,550 per baht weight and selling price Bt28,650, while gold ornaments cost Bt28,030.84 and Bt29,150, respectively.

At close on Thursday (August 13), the buying price of a gold bar was Bt28,250 per baht weight and selling price Bt28,350, while gold ornaments cost Bt27,742.80 and Bt28,850, respectively.

The Comex (Commodity Exchange) gold price to be delivered in December rose by US$21.4 or 1.1 per cent to $1,970.4 (Bt61,180.83) per ounce at Thursday’s close.

Gold price skyrocketed from mass buy-ups as a safe-haven asset due to uncertainty following the weakening dollar, the negotiations on a US economic stimulus package and the high number of US jobless claims.

The baht opened at 31.06 to the US dollar on Friday morning (August 14), unchanged from Thursday’s close.

The Thai currency is expected to move between 30.95 and 31.15 today, said Jitipol Puksamatanan, head of Markets Strategy at SCB Securities.

On Thursday night, the financial markets moved in a narrow range. The S&P 500 decreased by 0.2 per cent, while Stoxx Europe 600 fell by 0.6 per cent.

This movement was caused by investors’ speculation, after the failure in the finalisation of US financial policies.

However, the market was supported by economic numbers. The initial jobless claims recently decreased to around 963,000 positions. Also, total claimants fell to 15.4 million people, showing that the US economy is recovering.

In the fluctuating financial market, the dollar weakened by 0.1 per cent, compared to other main currencies. Moreover, the US Ten-Year Treasury yield reached 0.7 per cent.

Meanwhile, the baht moved in a narrow range, as the movement of capital markets in Asia was not clear — whether it was positive or negative. The strategist believed that the main factor to affect the baht in the future would be the restart of businesses in the service sector around the world.

He added that the weak points of the baht were Thai political instability and slow economic recovery. These two issues obstructed capital flows into the country, he explained.

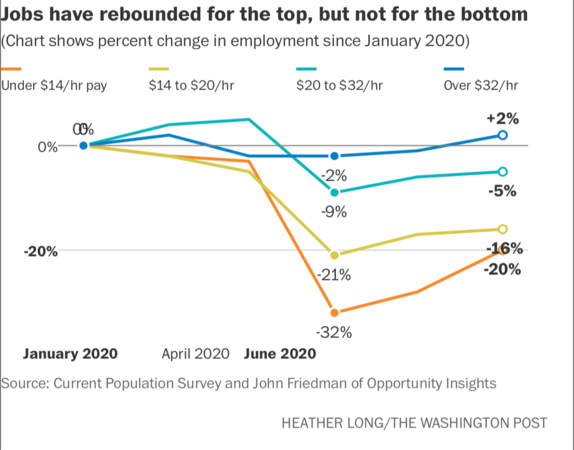

The recession is over for the rich, but the working class is far from recovered

EconAug 14. 2020Jobs have rebounded for the top, but not for the bottom Photo by: Heather Long — The Washington Post

By The Washington Post · Heather Long · NATIONAL, BUSINESS

U.S. stocks are hovering near a record high, a stunning comeback since March that underscores the new phase the economy has entered: The wealthy have mostly recovered. The bottom half remain far from it.

This dichotomy is evident in many facets of the economy, especially in employment. Jobs are fully back for the highest wage earners, but fewer than half the jobs lost this spring have returned for those making less than $20 an hour, according to a new labor data analysis by John Friedman, an economics professor at Brown University and co-director of Opportunity Insights.

Though recessions almost always hit lower-wage workers the hardest, the pandemic is causing especially large gaps between rich and poor, and between white and minority households. It is also widening the gap between big and small businesses. Some of the largest companies, such as Nike and Best Buy, are enjoying their highest stock prices ever while many smaller businesses fight for survival.

Some economists have started to call this a “K-shaped” recovery because of the diverging prospects for the rich and poor, and they say policy failures in Washington are exacerbating the problems.

Congress has not passed another relief bill, and the bulk of the federal stimulus originally passed in March to sustain small businesses and more than 28 million people on unemployment benefits has largely expired.

As talks between Republicans and Democrats in Washington have disintegrated, the burden of supporting the economy has fallen on the Federal Reserve, which has pumped trillions of dollars into the financial system to prop up businesses and markets, fueling a 50 percent gain in the stock market since March and a surge in home and car buying. But the Fed’s main tools in this situation are reducing the benchmark interest rate and buying bonds. The Fed cannot give people checks, which is why its actions have done little to help renters facing eviction or small businesses on the verge of dying.

Fed leaders have urged Congress to act swiftly before the damage to the economy becomes permanent. Boston Fed President Eric Rosengren warned on Wednesday that “the recovery may be losing steam.” Former Fed chair Janet Yellen called for “urgent” fiscal action.

“The stock market isn’t the economy. The economy is production and jobs, and there are shortfalls in virtually every sector of the economy,” Yellen said in an interview with The Washington Post.

“This pandemic is causing suffering and losses,” Yellen said. “Individuals and businesses are not going to make it through this unless they get grants, and only the federal government can do that.”

As much of the economy has moved to work-from-home mode, the shift has mainly benefited college-educated employees who do most of their work on computers. A Fed survey found that 63 percent of workers with college degrees could perform their jobs entirely from home, while only 20 percent of workers with high school diplomas or less could work from home.

Wealthier Americans also have seen their wealth recover – or even surge – as home values have jumped to their highest level ever (even in inflation-adjusted terms), according to the National Association of Realtors.

New analysis by Opportunity Insights of Labor Department data found employment is still 20 percent below pre-pandemic levels for workers earning under $14 an hour, and 16 percent down for those making $14 to $20 and hour. Opportunity Insights also analyzed data from the payroll processors Paychex, Intuit and Earnin and came to a similar conclusion.

“The recession is nearly over for high-wage workers, but low wage workers are no more than half-recovered,” said Friedman, who led the research, which is sponsored by Harvard and Brown universities and the Bill & Melinda Gates Foundation.

The pandemic and economic crisis have hit Black and Hispanic neighborhoods the hardest. Many of these households had little savings before the pandemic, and their jobs have been slower to return as the coronavirus risk remains highest in crowded indoor spaces such as shopping malls.

Black men and women have recovered about 20 percent of the jobs they lost in the pandemic vs. almost 40 percent for White men and 45 percent for White women, Labor Department data shows.

The slow job rebound is leaving many minority families fearful of eviction. Nearly half of Hispanic renters and 42 percent of Black renters said they had “no confidence” or only “slight confidence” they could pay their August rent, according to a to a Census Bureau survey conducted July 16-21. On the social media site Reddit, unemployed Americans are posting harrowing accounts of their electricity being shut off, not being able to afford medication and being days from eviction.

In many parts of the country, a sense of helplessness and fatigue has set in as the virus continues to threaten people’s health and the economy, and families see little action by Congress. Small-business owners are accustomed to being nimble, but this level of uncertainty makes week-to-week planning nearly impossible.

“There’s always been huge disconnect between politicians and the working class. I wish they would pay attention and listen to what we actually need: more clear guidance and some more financial support,” said Derek Caskey, co-owner of Sawstone Brewing Co. in Morehead, Ky.

Sawstone Brewing is one of more than 5 million businesses that received Paycheck Protection Program grants this spring. The grant the brewery received enabled Caskey to keep paying his eight workers and shift his business model to takeout orders. But the PPP money has run out and business has not fully recovered.

“What’s saving us right now is outdoor seating. But when that isn’t feasible, what are we going to do?” Caskey said.

The stock market is telling a different story. Thanks to a wave of optimism about a possible vaccine and an economic recovery, as well as continued support from the Fed, many investors are doing quite well. The Standard & Poor’s 500-stock index is within a few points of hitting a record high. If it happens, it would be the fastest turnaround ever from a bear market, said Howard Silverblatt, a senior analyst at S&P Dow Jones Indices. The tech-heavy Nasdaq Composite Index has been in record-high territory for more than a month.

President Donald Trump has hailed the “tremendous” stock market gains as a sign of a “super” economic rebound.

“We’re in the middle of a pandemic and yet we’re going to be hitting records,” Trump said Thursday on Fox Business channel.

It’s a similar tale in housing. Families with jobs and savings are taking advantage of the lowest mortgages rates in U.S. history – below 3 percent – to buy bigger homes at bargain rates. Home purchases are up more than 20 percent, and refinancing is up nearly 50 percent from a year ago, according to the Mortgage Bankers Association.

White House economic adviser Larry Kudlow suggested Wednesday that the recovery is going so well that the economy may not need much more aid from the federal government.

“We are entering what I think is a self-sustaining economic recovery,” Kudlow said on Fox Business. “A rising tide does lift all boats.”

Trump’s Council of Economic Advisers issued a report Thursday highlighting that poverty probably declined in the spring because of the $1,200 stimulus checks and extra unemployment funding Congress and the White House approved.

But former Trump economic adviser Gary Cohn was one of several business leaders this week stressing that the U.S. economy is far from healthy and that the consequences of Congress’s inaction could sting for years. He said the stock market gains are a red flag signaling that small businesses are being crushed.

“The stock market continues to reflect big businesses increasing their market share during #COVID19. If a small business closes, a larger business fills the void. We need to contemplate what this means for Main Street USA going forward. Is this really the future we want?” Cohn tweeted.

Janice Tabangcura is one of millions of Americans furloughed and waiting to be called back to work. Tabangcura has been a line cook at Roy’s Waikiki Restaurant in Hawaii for six years. The normally vibrant Honolulu neighborhood is empty, and no one knows when that will change.

“It’s creepy. Waikiki is usually so busy. We call it Hawaii’s little New York. But now you see five people on the street,” Tabangcura said. “They keep extending the quarantine here. It’s dampening our spirits. We thought tourism would pick up this month, but it hasn’t.”

Tabangcura, 30, has waited weeks for an unemployment check, which still hasn’t come. To make some money and stay hopeful, she’s started a baking business, delivering “Bento boxes” of cookies and pastries.

For many of the unemployed, the downturn is turning out to be far longer than they had anticipated. Nearly 80 percent of furloughed or laid-off workers thought they would be rehired, a Washington Post-Ipsos poll conducted April 27-May 4 found. Yet so far, only 42 percent of jobs have returned, Labor Department data shows.

“This has been a very clear K-shaped recovery,” says Peter Atwater, an adjunct lecturer in economics at the College of William & Mary. “The biggest and wealthiest have been on a clear path toward recovery. Meanwhile, for most small business and those worst off, things have only become worse. The contrast is piercing: One group feels better than ever while the other borders on hopelessness.”

One of the key debates between Republicans and Democrats is about how long the U.S. economic recovery will take. Republicans point to the fact that the economy added more jobs than expected in May, June and July as a sign that a comeback is taking hold. They also highlight the swift bounce-back in home, car and truck sales. Some auto dealerships have had their best July ever, and gasoline sales have mostly rebounded.

Democrats point out that the unemployment rate is 10.2 percent – higher than at any point during the Great Recession, and that millions are unable to pay rent. Census data shows that more than half of Americans said they felt depressed or hopeless in July, and 20 percent of Hispanic households with children and nearly a quarter of Black households with children say they don’t have enough to eat.

One of the most telling indicators about the economy is consumer spending. It’s still down about 8 percent from pre-pandemic levels overall, but it was down only 2 percent among low-income households in July. This is largely because of the stimulus checks that went to working- and middle-class families this spring and the extra $600 a week in unemployment aid Congress sent out in April, May, June and July.

Now that those funds for struggling families have stopped, many economists predict a rapid rise in evictions, bankruptcies and vehicle repossessions – as well as a hit to the overall economy as spending slows.

Trump attempted to take action over the weekend to provide more aid to struggling Americans, but it was limited. Even if Trump’s executive moves survive legal challenges, they would, at best, pump less than $100 billion into the economy, JPMorgan notes. That’s far less than the $1 trillion or more that many on Wall Street and Main Street are counting on.

“The consensus is that a deal is necessary if the U.S. is to avoid economic calamity,” JPMorgan wrote in a morning note.

By The Washington Post · Hamza Shaban · BUSINESS U.S. stocks came close to making financial history Thursday, soaring toward record highs before slipping in late-day trading.

The Standard & Poor’s 500 index has been on a remarkable turnaround since late March, when equities markets got hammered by the economic calamity of the coronavirus.

The benchmark index – which offers a broader measure of the stock market than the Dow Jones industrial average – has been flirting with its February record of 3,386.15 for several trading days. It briefly topped that level Thursday before falling back.

The ferocity of the rebound has been underpinned by massive financial support from the federal government, said Nicole Tanenbaum of Chequers Financial Management, allowing investors to look toward an eventual recovery. “Economic data, while still at dire levels, is starting to show signs of stabilization, which, combined with a better than expected earnings season, is further fueling investor optimism despite an incredibly uncertain backdrop,” she said.

For individual investors whose exposure to the stock market is exclusively or partially tied to their 401(k) retirement plans, the recovery marks a return to pre-pandemic highs. “The average 401(k) holder is feeling pretty good right now,” Michael Farr, president of Farr, Miller & Washington, said in an interview. But he noted the jarring contrast between the soaring ambitions of Wall Street and the dire conditions for many businesses and households pummeled by the pandemic.

“We have seen this separation and disconnect that has been disconcerting to some investors where share prices continue to rise but the economic data and an economic recovery remains tepid,” he said. “You’re coming up on all-time highs when you still have 10 percent unemployed – that’s a huge deal.”

In the final hour of trading Thursday, the S&P 500 edged down 6.9 points, or 0.2 percent, to 3,373.43. The Dow gave up 80.12 points, or 0.29 percent, to settle at 27,896.72. The tech-heavy Nasdaq composite index, which has been buoyed by the tech giants and recently set its own record, advanced 30.26 points, or 0.3 percent, to 11,042.50.

The slight losses came as weekly jobless claims dipped below 1 million for the first time in four months, though they remain at historically high levels.

The U.S. Labor Department reported that 960,000 Americans filed for unemployment insurance last week, compared with 1.18 million the week before. Before the pandemic, the record stood at 695,000, which was set during the 1982 recession. Altogether, more than 28 million people are receiving some form of unemployment benefits, government data show.

The rising optimism on Wall Street clashes with other data highlighting the devastating effects of the pandemic. Wednesday marked the deadliest day of the summer as the United States recorded nearly 1,500 coronavirus deaths – the largest single-day count since mid-May and the latest signal that the contagion is far from under control.

U.S. stocks lost more than a third of their value between Feb. 19 and March 23, when the pandemic set off panic and weeks of wild intraday swings. The stunning turnaround continues to defy the entrenched recession and stalled efforts in Washington to pass another round of emergency relief.

Investors instead have focused on aggressive actions by the Federal Reserve and the Treasury, which have marshaled far more financial resources to stem the damage of the pandemic compared with their interventions during the Great Recession. They’ve also found room for optimism in corporate earnings that showed better-than-expected resilience, and the potential for a coronavirus vaccine.

By The Washington Post · Eli Rosenberg · NATIONAL, BUSINESS, US-GLOBAL-MARKETS WASHINGTON – About 960,000 workers filed for unemployment insurance last week, which marks the first time that initial claims dipped below 1 million since mid-March, when the coronavirus pandemic first took hold and workers were told to stay home.

The weekly claims figure for the week ending Aug. 8 fell below the 1.18 million claims from last week but remained well above historic highs. The pre-pandemic record for initial weekly claims was 695,000, from 1982, another recession.

Another 488,000 new claims were filed for Pandemic Unemployment Assistance, which is offered to gig and self-employed workers.

All told, more than 28 million people are currently receiving some form of unemployment benefits as of the week of July 25, down more than 3 million from the previous week.

Economist said that the longer the pandemic drags down the economy, the more job losses will become permanent – and the more likely that people filing weekly claims are not going to bounce back and be rehired, as many were earlier in the pandemic.

“We’re finally below 1 million, so that’s something to celebrate,” said Beth Ann Bovino, the chief economist at S&P Global Ratings Services. “But it stops there. The worry I have is that the times of quick recalls are in the past. I suspect that these jobs being lost are permanent, and that’s a real problem for the economy and for these households.”

The numbers come as economic issues take increased prominence in the presidential election. President Donald Trump has been touting the numbers of jobs that have been regained in the last three months, despite the unemployment rate and weekly claims remaining around historic highs.

Congress continues to be deadlocked in negotiations over extending the extra federal unemployment benefits that expired at the end of July. Economists have warned about the damage to the economy if those enhanced benefits, which many workers credit with helping them keep up to date on basic payments of rent and groceries, are not renewed.

Trump on Saturday issued an executive order that he claimed would enhance unemployment benefits by circumventing Congress, but the order raises questions about legality and how it would be implemented by the states. It’s unclear whether it will affect unemployment insurance in the near future.

Prime Minister Prayut Chan-o-cha will chair the first meeting of a new panel tasked with managing the economy amid the virus crisis on August 19, said Thai Chamber of Commerce chairman Kalin Sarasin. The opening meeting will evaluate the economic situation, he said.

The committee will hear private sector proposals that the government urgently launch measures to bridge the economic gap, solve unemployment, help small business operators survive the outbreak and boost domestic tourism.

The PM on August 13 announced the panel was being formed to deal with the economic impact of Covid-19. The committee will be chaired by Prayut and run by 22 members – 11 ministers plus the Bank of Thailand governor and representatives from the Federation of Thai Industries, the Thai Bankers’ Association and the Thai Chamber of Commerce.

Prayut divvies up responsibilities among his six deputies

EconAug 13. 2020Newly appointed Energy Minister Supattanapong Punmeechaow, right, will also oversee the Finance Ministry in his capacity as deputy PM.

By The Nation

Prime Minister Prayut Chan-o-cha on Thursday (August 13) signed an order assigning responsibilities for all six deputy prime ministers, the government’s deputy spokesperson Traisulee Traisoranakul said.

According to Prayut’s orders, newly appointed Deputy PM and Energy Minister Supattanapong Punmeechaow will also look after the Finance Ministry, Board of Investment and the National Economic and Social Development Council, while incumbent Foreign Minister Don Pramudwinai, who has just been named deputy PM, will also oversee the Ministry of Higher Education, Science, Research and Innovation.

Incumbent Deputy PM Prawit Wongsuwan will be in charge of four ministries, namely Digital Economy and Society, Natural Resources and Environment, Interior and Labour, and will also oversee the National Intelligence Agency and the National Security Council.

Deputy PM Wissanu Krea-ngam will also oversee four ministries, namely Justice, Culture, Education and Industry, as well as the government’s Public Relations Department.

Current Public Health Minister Anutin Charnvirakul, will be in charge of two additional ministries in his capacity as deputy premier, namely Tourism and Sports and Transport.

Incumbent Commerce Minister Jurin Laksanawisit will as deputy PM also oversee the Social Development and Human Security Ministry and the Agriculture and Cooperatives Ministry.

New Higher Education Science, Research and Innovation Minister Anek Laothamatas

Meanwhile, new Higher Education Science, Research and Innovation Minister Anek Laothamatas said on Thursday that his first job will be to create employment opportunities for new graduates. He added that his ministry will have to adjust its policies to serve the demand of students instead of setting its own policies for them to follow.

He said he will also focus on upskilling and reskilling of workers, with the aim of turning his ministry into the country’s brain. He also said that larger sums will be allocated for research and development.

The PM today also announced the establishment of an economic situation management panel to deal with the Covid-19 fallout.

PM Prayut Chan-o-cha

The panel will be chaired by Prayut and run by 22 members – 11 ministers plus the Bank of Thailand governor and representatives from the Federation of Thai Industries, the Thai Bankers’ Association and the Thai Chamber of Commerce.

It will draw up directions for economic recovery and follow up on progress of their implementation.

Provincial-level committees were also set up to advise governors of provinces on developing projects to benefit local people.

The Stock Exchange of Thailand (SET) Index rose 9.85 points or 0.74 per cent, closing at 1,346.69 today (August 13), with transactions totalling at Bt77.812 billion with an index high of 1,353.53 and a low of 1,343.09.

In the morning session, a stock analyst at Krungsri Securities said he expected the index to rise between 1,345 and 1,350 before falling as Russia has claimed to have successfully developed a Covid-19 vaccine, while the price of oil rose to more than US$42 (Bt1,305) per barrel.

However, the analyst said the index will still be under pressure from uncertainty following a planned $1-trillion economic stimulus package in the US and US-China trade negotiations on Saturday.

The top 10 stocks with the highest trade value today were KBANK, AOT, BBL, KCE, STGT, MINT, PTT, SCB, HANA and CPALL.

As of 4.30pm, the price of crude oil had risen by $0.13 or 0.30 per cent to $42.80 per barrel, while gold dropped by $4.80 or 0.25 per cent, to $1,944.20 per ounce.

Other Asian indices were mixed:

Japan’s Nikkei Index closed at 23,249.61, up 405.65 points, or 1.78 per cent.

China’s Shanghai SE Composite Index closed at 3,320.73, up 1.46 points, or 0.044 per cent, while Shenzhen SE Component Index closed at 13,291.32, down 17.20 points, or 0.13 per cent.

Hong Kong’s Hang Seng Index closed at 25,230.67, down 13.35 points, or 0.053 per cent.

South Korea’s KOSPI Index closed at 2,437.53, up 5.18 points, or 0.21 per cent.

Taiwan’s TAIEX Index closed at 12,763.13, up 92.78 points, or 0.73 per cent.

The Department of Trade Negotiations will urge the Cabinet in October to consider signing the Regional Comprehensive Economic Partnership (RCEP) pact, the department’s director general Auramon Supthaweethum said.

She added that the vetting of all 20 chapters of the accord had been completed and that it can be signed during the Asean Summit in November, which will be held in Vietnam.

After the signing, Thailand will have to undertake a parliamentary process to rectify the deal. The agreement is expected to come into force by mid next year.

RCEP covers 16 countries – the 10 members of Asean plus the six countries that the grouping has free trade agreement (FTA)s with, namely Australia, China, India, Japan, South Korea and New Zealand.

However, India has not signed the RCEP accord as of now.

She said the department was educating Thai farmers and business owners on how they can benefit from the agreement.

The Commerce Ministry is also studying plans to set up a fund to compensate parties affected by Thailand’s FTAs with foreign countries or free-trade blocs.

Thailand exported $1.14 billion (Bt35.43 billion) worth of fresh durian to global markets in the first half of the year, or 69 per cent of total fruit exports, the Department of Trade Negotiation said, citing statistics.

Director-general Auramon Supthaweethum said total durian exports in the January-June 2020 period grew a huge 73 per cent compared to the first half last year.

The top export market for durian was China, amounting to $1.02 billion in value. Durian exported to the Asian giant accounted for 73 per cent of total durian exports, increasing by a whopping 140 per cent compared to the same period in 2019.

Durian exported to Hong Kong and Asean represented 15 per cent and 12 per cent of the total, with a respective value of $207 million and $164 million.

Vietnam was the main Asean export market, Auramon said, adding that durian exports to Hong Kong rose by 34 per cent and to Asean 25 per cent.

Auramon mentioned that free trade agreements (FTAs) were important for the growth of durian exports, since it allowed the fruit to be exempted from tax, making it more competitive in foreign markets.

Thailand has FTAs with nine other ASEAN states, China, Hong Kong, Australia, New Zealand, Japan, India, and Chile. The country earned total revenue of $1.39 billion from exporting durian to its FTA partners.

Jobs have rebounded for the top, but not for the bottom Photo by: Heather Long — The Washington Post

Jobs have rebounded for the top, but not for the bottom Photo by: Heather Long — The Washington Post

Prime Minister Prayut Chan-o-cha

Prime Minister Prayut Chan-o-cha  Newly appointed Energy Minister Supattanapong Punmeechaow, right, will also oversee the Finance Ministry in his capacity as deputy PM.

Newly appointed Energy Minister Supattanapong Punmeechaow, right, will also oversee the Finance Ministry in his capacity as deputy PM. .jpeg)

The department’s director-general Auramon Supthaweethum

The department’s director-general Auramon Supthaweethum