The price of gold in Thailand on Monday morning was unchanged from Saturdays one-time trading price announcement.

A9.28am report from the Gold Traders Association showed the buying price of gold bar at THB28,550 per baht weight and selling price at THB28,650, while the buying and selling price of gold ornaments is THB28,030.84 and THB29,150, respectively.

The spot gold price on Monday morning was moving around US$1,794 (THB60,475) per ounce after Comex gold at close on Friday rose slightly by $1.2 to $1,785.5 per ounce due to support in buying gold as a safe-haven asset amid concerns about the new variant of Covid-19 virus in South Africa.

Krungsri Securities forecast the Stock Exchange of Thailand (SET) Index on Monday (November 29) would fall to between 1,590-1,600 points.

It said the index is currently under pressure due to uncertainty over the latest Omicron Covid-19 variant in Africa and the fresh coronavirus wave in Europe.

It added that the abovementioned negative sentiment also caused the oil price to drop sharply.

“Hence, we advise buying stocks which gained specific positive sentiment,” Krungsri Securities said.

It also recommended buying of the following companies’ shares as an investment strategy:

▪︎ BCH, CHG, MEGA, STA and STGT, which benefit from the Covid-19 crisis.

▪︎ HANA, KCE, TU, ASIAN, NER, EPG and XO, which benefit from the weakening baht.

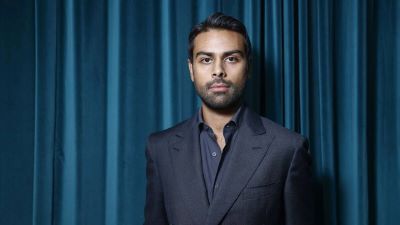

Karam Hinduja has rather un-Swiss ambitions for the Swiss private bank he took charge of last year.

The 31-year-old grandson of Srichand Hinduja, the patriarch of the $18 billion British-Indian Hinduja Group, says he wants to stay true to his grandfather’s values while trying to remake the bank to attract a more modern, less stuffy clientele. In an interview at the bank’s Geneva headquarters, Karam said he told his employees to be more like the bank’s clients, who may just as likely have made their fortunes as tech entrepreneurs as from finance.

“If your client is in shorts, t-shirt and a pair of flip flops, feel free to do the same, meet them at their level,” the executive said.

Karam has taken over the bank at a difficult juncture for the Hindujas, with a deepening dispute between his ailing 85-year-old grandfather’s side of the family and Srichand’s three younger brothers. It doesn’t help that the bank sits at the heart of the conflict. In a legal battle, Srichand — represented by his daughter Vinoo — is claiming sole ownership of the bank. SP’s brothers say the bank is part of the Hinduja Group.

Karam took charge in early 2020, a year which saw client assets drop by more than 30% from just two years earlier to 1.69 billion Swiss francs ($1.82 billion). The declines were due to drops in asset values not client withdrawals. Total assets under management rebounded to 2.43 billion Swiss francs as of the end of October.

Karam renamed the bank SP Hinduja Banque Privee, although on the Hinduja Group website it is still called Hinduja Bank Switzerland. The executive sometimes fields calls about the family dispute from those who know his grandfather but says it’s more “noise” than anything else and says he’s focused on the charting the bank’s future.

“I’m aware of the dynamics that are occurring at the family level, but I’m here to try and build a fantastic financial institution,” he said in an East Coast accent honed over a decade in New York as an undergraduate at Columbia University and then in venture capital.

While in the U.S., he came close to choosing another career path, spending a year at Nick Bollettieri’s elite tennis academy in Florida in a bid to go pro. That was derailed by a herniated disc and the realization that he wouldn’t make the cut. He’s now back in Europe to take part in the family business.

At the bank, he could not be more different than his predecessor, Gilbert Pfaeffli, a former Swiss Army colonel who’d spent three decades at UBS. Pfaeffli was hired in 2016 in the wake of a pair of bad investments in commodity trading that lost the bank a reported 25 million Swiss francs.

“There was a lack of control, there was a lack of order,” said Karam. Pfaeffli “was the perfect person, with the background he has, to bring in that very military style to the institution.”

The bank was stripped of its Cayman Island banking license in May 2020 for failing to meet anti-money laundering compliance rules. That unit was already being wound down at the time and has since been closed, Karam said. The bank also faces two claims totaling 6 million Swiss francs from unidentified former clients “alleging breaches of the bank’s duties,” according to its annual report.

Karam has brought four people to Geneva from Timeless Media, a digital media company he founded in New York, and a similar number of Srichand’s advisers from London to shake things up.

“I haven’t come from the traditional world of finance,” said Karam, dressed in a black suit and matching black open-necked shirt. “I’ve done dealmaking, I’ve done investing but I haven’t come from the banking grassroots.”

The bank introduced Climate Action Portfolio, a fund focused on alternative energy investments to attract a different kind of investor. Hinduja said he plans more forays into India, where younger entrepreneurs from Indian families who had left the country are now returning.

“Industry is moving in India. Markets are moving. There’s a lot of opportunity,” he said.

The Stock Exchange of Thailand (SET) Index closed at 1,610.61 on Friday, down 37.85 points or 2.30 per cent. Transactions totalled 123.47 billion baht with an index high of 1,640.91 and a low of 1,608.55.

The index dropped for the second day running after falling by 1.36 points or 0.08 per cent on Thursday.

The 10 stocks with the highest trade value today were KBANK, AOT, SCB, CPALL, BANPU, BBL, PTTGC, EA, PTT and TTB.

Other Asian indices were on the fall:

Japan’s Nikkei Index closed at 28,751.62, down 747.66 points or 2.53 per cent.

China’s Shanghai SE Composite closed at 3,564.09, down 20.09 points or 0.56 per cent, while the Shenzhen SE Component closed at 14,777.17, down 50.78 points or 0.34 per cent.

Hong Kong’s Hang Seng Index closed at 24,080.52, down 659.64 points or 2.67 per cent.

South Korea’s KOSPI Index closed at 2,936.44, down 43.83 points or 1.47 per cent.

Taiwan’s TAIEX Index closed at 17,369.39, down 284.80 points or 1.61 per cent.

The baht opened at 33.43 to the US dollar on Friday, weakening from Thursday’s closing rate of 33.36.

The Thai currency is likely to move between 33.35 and 33.50 to the greenback during the day, Krungthai Bank market strategist Poon Panichpibool predicted.

Poon said that the baht is weakening after the foreign investors had sold 4 billion baht of short term bonds in two days. They cut their loss as the baht might reach the level at 33.50 to the dollar.

Meanwhile, Poon suggested speculating the dollar because it might be sold after the dollar is strengthening and reached the resistance level. The dollar might go down in the short term if there is no new factor to support the dollar. However, the Covid-19 situation might support the dollar in this period.

Poon believed that the baht will reach the key resistance level of 33.45 to 33.50 to the dollar which is the level at which exporters are waiting to sell the dollar and foreign investors are buying the baht. Moreover, the baht might strengthen if the gold price goes up.

The support level of baht will be from 33.10 to 33.20 to the dollar which exporters are buying the dollar.

The price of gold rose by THB100 in morning trade on Friday.

AGold Traders Association report at 9.25am said the buying price of a gold bar was THB28,350 per baht weight and selling price THB28,450, while the buying and selling price of gold ornaments is THB27,833.76 and THB28,950, respectively.

At close on Thursday, the buying price of a gold bar was THB28,250 per baht weight and selling price THB28,350, while gold ornaments were THB27,742.80 and THB28,850, respectively.

The spot gold price on Friday morning hovered around US$1,792 (THB60,126) per ounce after the Comex gold market closed on Thanksgiving yesterday.

Krungsri Securities forecast the Stock Exchange of Thailand (SET) Index on Friday (November 26) would fluctuate between 1,640-1,660 points.

It said the index is currently under pressure due to uncertainty over a new Covid-19 variant in Africa, as well as a fresh Covid-19 wave in Europe.

It added that the US Federal Reserve signalling it would raise the interest rate and taper its quantitative easing programme sooner than expected in order to deal with inflation would also pressure the index.

“However, mass-buy ups of stocks which gained specific positive sentiment would help boost the index,” Krungsri Securities said.

It also recommended buying of the following companies’ shares as an investment strategy:

▪︎ BANPU and AGE, which benefit from rising coal price.

▪︎ HANA, KCE, TU, ASIAN, NER, EPG and XO, which benefit from the weakening baht.

▪︎ BBL, TTB, KTB, KBANK and BLA, which would benefit from the rising interest rate.

A new data protection law is changing the calculus for doing business in China, with foreign and domestic firms scrambling to comply, and some companies including LinkedIn and Yahoo choosing to leave.

China’s personal information protection law, implemented this month, is the latest factor adding to a challenging political environment for businesses operating in the country and altering the cost-benefit analysis. While the untapped business potential of 1.4 billion consumers was once an irresistible draw, this is increasingly changing.

James Zimmerman, a Beijing-based American lawyer, said that the China market had become “less and less palatable for Western companies” because of “reputational risks of operating in an environment with extreme content censorship, and tighter regulatory conditions.”

The trade war brought politics into U.S.-China business to a much greater degree, with Beijing and Washington wielding tariffs and consumer product boycotts in their power struggle. Domestically, Beijing has launched a populist campaign against big business, effectively making the market less profitable for many companies under stricter new regulations.

And for some Western business executives, the human-rights controversies of President Xi Jinping’s era have become a bridge too far, including a crackdown on ethnic minorities in the Xinjiang region that Washington classified as genocide; silencing of Hong Kong protesters through use of force and imprisonment; and, most recently, the disappearance of tennis star Peng Shuai after she accused a former top official of sexual assault.

Women’s Tennis Association Chairman Steve Simon said last week the organization is willing to cease its China operations, potentially losing hundreds of millions of dollars, if Chinese authorities don’t properly investigate Peng’s allegations.

On Nov. 2, the same day the allegations appeared on Peng’s verified social media account, Yahoo announced it was pulling out of the China market due to “the increasingly challenging business and legal environment.” Days earlier, LinkedIn had also cited a significantly more challenging operating environment in its decision to close the Chinese version of its networking site, though it said it would keep a simple China job listing site without a social feed or the capability to share articles.

Yahoo had been downsizing its China operations for years, faced with diminishing business in the country because of censorship and competition from local players. In 2007, the company came under intense criticism in the United States for turning over emails of two Chinese political dissidents to Beijing authorities, which were used as evidence in their prosecution; they were later imprisoned. Yahoo shut down its email service in China in 2013 and closed its Beijing office in 2015.

Still, the company hung on in the China market until now. While Yahoo didn’t go into details about its reasons for leaving China, its announcement occurred as the new data protection law came into effect Nov. 1, which industry executives said would require multinational companies to make significant and costly changes to their processing and storage of data.

The law has broad consumer-protection measures that limit companies – Chinese and foreign – from collecting consumers’ personal information without their consent, and from storing more personal data than necessary. It also restricts the transport out of the country of Chinese nationals’ personal data, an especially onerous restriction for multinational tech companies.

“It’s created a lot of uncertainty,” said Lester Ross, policy head of the American Chamber of Commerce in China, about the new personal data law. He said AmCham has been communicating with Chinese regulators to request a period of forbearance to give U.S. companies more time to comply.

Clarisse Girot, Asia-Pacific director of the Future of Privacy Forum, said the Chinese law is largely modeled on Europe’s General Data Protection Regulation, implemented in 2018. But she said China’s version diverges from GDPR in its stipulations for China’s national sovereignty over data, instead of being purely about consumer rights.

The law also comes amid broad pressure on businesses from Xi’s “common prosperity” campaign, a populist push to narrow the country’s wealth gap. A number of China’s most powerful companies have come under regulatory crackdown over the past year, and businesses have scrambled to make large philanthropic donations to prove they are supportive of the government effort.

U.S. video game maker Epic Games gave up its pursuit of the China market on Nov. 15, several months after Beijing banned children from playing video games on school nights. Epic’s popular game Fortnite had been available on a trial basis in China for more than two years, but it failed to gain regulatory approval for a formal release.

The departure of some foreign tech companies means less competition for local players, but it could bring longer-term challenges. China has benefited from the presence of leading overseas high-tech companies, which has helped advance the nation’s technological know-how through joint-ventures and tech transfer agreements.

Ross said that China’s strict entry restrictions during the pandemic have been yet another challenge for business, as has an energy crunch that has disrupted factory production across the country. He said he hasn’t heard of any foreign executives receiving quarantine exemptions while entering China, unlike some other Asian countries, such as South Korea, that have allowed exemptions for business trips.

Several smaller American companies that were considering entry into the China market have shelved those plans because of the country’s coronavirus restrictions, Ross said, without identifying them.

Most nonessential travel into and out of China is still prohibited, and those able to travel to the country must complete at least three weeks in quarantine. In one northern Chinese city, Shenyang, the quarantine length was extended this month to a whopping 56 days, in a strong deterrent against visitors.

The Thai government has pledged to support the private sectors transition to a low carbon economy and make sure that the shift is smooth and has minimal impact, with an emphasis on the Bio-Circular-Green Economy (BCG) Model to help tackle climate change.

KPMG has conducted the first-ever Net Zero Readiness Index (NZRI) to assess countries’ readiness to transition to Net Zero. Oil-rich Nordic nation deemed ‘most prepared’ and ‘ready’ to reach Net Zero by 2050.

• Northern Europe dominates top spots, with Norway ranked number one, and UK and Sweden in second and third place.

• A lack of delivery capability is a weak point in global Net Zero emissions ambitions.

• Thailand deemed as ‘country to watch’ in achieving Net Zero, being one of seven countries seeing significant opportunities to advance their decarbonization efforts through large-scale projects and emerging escalation initiatives

The report compares the progress of a selection of countries in reducing the greenhouse gas emissions that cause climate change and assesses their preparedness and ability to achieve Net Zero by 2050. The date 2050 was proposed by the United Nation’s (UN) Intergovernmental Panel on Climate Change, which said that cutting net emissions by about 45 percent from 2010 to 2030, then 100 percent by 2050 would limit temperature rises to 1.5 degrees Celsius. In August 2021, a total of 195 governments said that humanity has already warmed the planet by approximately 1.1 degrees Celsius; that 1.5 degrees is likely to be reached or exceeded in the next two decades; and that without immediate, rapid and large-scale reductions in emissions, limiting warming to 1.5 or even 2 degrees will be beyond reach.

Using 103 indicators, recognized as key drivers to achieving Net Zero, the top 25 performing countries and seven ‘countries to watch’ were identified.

Despite being one of the world’s largest oil and gas exporters, Norway topped this year’s NZRI, partly due to private and public investment in renewable energy and electrified transport across the country. In 2016, the Norwegian parliament voted to bring forward its target date for carbon neutrality from 2050 to 2030. However, despite their top ranking, the nation still faces significant decisions over how it continues to tackle challenges in their transition to net zero.

The UK, which is hosting the COP26 Climate Summit this month, took overall second place, due in-part to cross-party political support and clear legally-backed targets that have enabled the comparatively swift decarbonization of the country’s power generation sector, but many obstacles remain – particularly on heat and buildings.

Key findings from the Index include:

• Some countries are lagging in adopting Net Zero with only 9 of those surveyed, who account for approximately 8 percent of global emissions, having legally binding commitments in place. In order to stimulate delivery capability at the sector level, these targets need to be backed by robust strategies, policies and support mechanisms. In most jurisdictions the NZRI preparedness on a national level is mirrored by the level of readiness at the sector level.

• A lack of delivery capability is a weak point in global Net Zero ambitions. The Index shows that those countries with a Net Zero target in place, either legally binding or policy, demonstrate stronger capability across sectors. The report also shows a correlation between prosperity and the readiness to achieve Net Zero, highlighting the need to escalate the mobilization of support to developing economies.

• Insights from all surveyed nations show that whilst the global financial sector is increasingly factoring climate risk into their investment and lending decisions, governments have a critical role to play in enhancing access to such financing by creating enabling environments such as sustainable finance strategies, policies and regulatory frameworks.

• These country insights also help to highlight the importance of political alignment and public support in the success of key decarbonization initiatives.

The NZRI top 25 countries are:

Rank

Country

Rank

Country

1

Norway

14

USA

2

United Kingdom

15

Singapore

3

Sweden

16

Chile

4

Denmark

17

Australia

5

Germany

18

Brazil

6

France

19

Poland

7

Japan

20

China

8

Canada

21

Malaysia

9

New Zealand

22

Argentina

10

Italy

23

Mexico

11

South Korea

24

Turkey

12

Spain

25

UAE

13

Hungary

KPMG also listed seven countries to watch as these countries are seeing significant opportunities to advance their decarbonization efforts through large-scale projects and emerging escalation initiatives:

• India

• Indonesia

• Nigeria

• Russia

• Saudi Arabia

• South Africa

• Thailand

Thailand has plans to achieve carbon neutrality by 2050 and net zero emission by 2065 under a new energy plan that could see renewable energy account for a 50% share of its new power generation We have seen this translated into several initiatives such as only zero-emission vehicles being allowed to register as new vehicles from 2035 onwards. The Thai government has pledged to support the private sector’s transition to a low carbon economy and make sure that the shift is smooth and has minimal impact, with an emphasis on the Bio-Circular-Green Economy (BCG) Model to help tackle climate change.

Tanate Kasemsarn, Head of ESG, KPMG in Thailand

“The last few years have seen increasing public awareness of climate change in Thailand, partly due to the government adding the subject to the education curriculum,” says Tanate Kasemsarn, Head of ESG, KPMG in Thailand. “This is progress in the right direction as we are creating a generation that is aware of the importance of climate change. At KPMG, we believe in working together towards a more sustainable future and we can only achieve that with not only the commitment of the public sector, but also of the private sector.

Ganesan Kolandevelu, Head of Climate Change and Sustainability Services, KPMG in Thailand

“Thailand will need to improve research capacity, especially in harder-to-decarbonize sectors,” says Ganesan Kolandevelu, Head of Climate Change and Sustainability Services, KPMG in Thailand “Technologies such as those that can measure the emission of greenhouse gas, will help the country achieve its climate change agenda. This will need cooperation from all stakeholders. For businesses, having a clear ESG agenda should not just be a ‘tick-the-box’ activity. There are real added benefits from being a sustainable business, and this includes increasing confidence of stakeholders and loyalty from consumers.”

Natthaphong Tantichattanon, Partner, Climate Change and Sustainability Services, KPMG in Thailand.

“Another point for companies in Thailand to consider is the Securities and Exchange Commission (SEC)’s requirement for the ‘One Report’ for reporting year 2021 that gives more focus on the disclosure of sustainability and ESG,” says Natthaphong Tantichattanon, Partner, Climate Change and Sustainability Services, KPMG in Thailand. With increased requirements for sustainability disclosure, companies must now disclose their sustainability strategy, policy and targets, value chain issues, environmental impact, Greenhouse Gas disclosure and social engagement. Companies must now include ESG in their strategy and business development and should start planning accordingly on how they will achieve this.”

The publication of the Net Zero Readiness Index came ahead of November’s crucial COP26 Climate Summit in Glasgow. The United Nations outlines that greenhouses gases in the atmosphere are at their highest level for three million years, driving a global temperature increase of 0.85 degrees Celsius between 1880 and 2012 and a rise in sea-levels of 19cm. Political and business leaders are becoming increasingly aligned that immediate action is required to stop the catastrophic social, environmental and economic impacts further temperature rises could have on the planet.

Today H.E. General Prayut Chan-o-cha, Prime Minister of Thailand, attended a virtual executive meeting with Mr. Ren Zhengfei, CEO of Huawei Technologies.

Today H.E. General Prayut Chan-o-cha, Prime Minister of Thailand, attended a virtual executive meeting with Mr. Ren Zhengfei, CEO of Huawei Technologies. H.E. Gen Prayut expressed appreciation for Huawei’s continued support of Thailand’s digital transformation and post-pandemic recovery, and his eagerness to further strengthen cooperation with Huawei to promote the Thailand 4.0 strategy and digital talent cultivation.

During the meeting, Gen Prayut and Mr. Ren exchanged views on how to consolidate digital competitiveness and build a stronger foundation for ICT talent in Thailand. Participants included XXX, Simon Lin, President of Huawei Asia Pacific, and Abel Deng, CEO of Huawei Thailand.

Gen Prayut also stressed the important role that advanced ICT technologies and digital innovation would play in supporting Thailand’s economic resilience and sustainability, stating that “Huawei has provided profound contributions to Thailand’s fight against the pandemic and the country’s digital transformation. I am deeply impressed by Huawei’s history and dedication. Going forward, Thailand is eager to continue working with Huawei in various areas, including the digital economy, 5G Smart Hospitals, cloud and computing, digital power, smart logistics, and further data centers.”

Thailand Prime Minister Meets Huawei CEO to Promote Collaboration on Digital Transformation and Talent Development

Mr. Ren expressed his gratitude for the Thai government’s trust in Huawei and congratulated Thailand on its successful 5G rollout. He emphasized that “Huawei and Thailand have been working together to build a strong digital infrastructure foundation for many years. We look forward to further accelerating the integration digital technologies in Thailand’s key industries, especially in port and airport capabilities.”

“We strongly believe in Thailand’s successful digital transformation and talent development. Our local team will continue working closely with Thai customers and partners to serve the country’s social and economic development with technology solutions.” Ren said.

Driving towards Thailand’s digital blueprint of becoming the ASEAN digital hub, Huawei and Thailand have been closely cooperating in two key areas.

First, in line with the Thailand 4.0 strategy, Huawei has worked with its customers to accelerate Thailand’s digital transformation and ICT infrastructure innovation. Through the adoption of 5G, Cloud, and AI, Huawei and its industry partners are enabling Thailand’s key sectors and creating exciting opportunities across multiple sectors, including healthcare, education, transportation, e-government, and smart city, to bolster Thailand’s long-term socioeconomic development and digital ecosystem.

Alongside this, the session flagged the important potential cooperation of Huawei and Thailand on smart ports and airports. Mr. Ren introduced the company’s best practices regarding Smart Port and Smart Airport Solutions in China, where it builds automation capabilities based on all factors — people, vehicles, goods, enterprises, and places — to help build safe, efficient, and intelligent world-class ports and airports.

Thailand Prime Minister Meets Huawei CEO to Promote Collaboration on Digital Transformation and Talent Development

Secondly, Gen Prayut and Mr. Ren also highlighted their commitment to cultivate and upskill digital talent in Thailand in order to drive Thailand’s digital transformation and long-term development. Both men stressed that the public and private sector must work together to build an open, shared ICT talent ecosystem that benefits all.

Aimed at cultivating Thailand’s ICT talent and digital workforce, Huawei established the Huawei ASEAN Academy (Thailand) in 2019, which has since trained over 41,000 ICT professionals and provided training to 1,300 small and medium-sized enterprises. Huawei has also signed MOUs with more than 20 Thai universities. With a digital world fast approaching, Huawei is determined to ensure that no one is left behind through digital inclusion initiatives that enhance the digital knowledge and employment prospects of vulnerable groups.

Since its establishment in Thailand in 1999, Huawei has fulfilled its mission to “Grow in Thailand, Contribute to Thailand” by continuously working to support Thailand’s digital transformation journey and contribute value to society. Huawei Thailand currently has over 2,800 employees, 86% of whom are local employees, and indirectly generates more than 8,500 job opportunities. In March 2021, Huawei Thailand was chosen for the Special Prime Minister Award as the “Digital International Corporation of the Year”, with the award recognizing Huawei for its valuable support and outstanding contributions to Thai society, as well as its efforts to support digital transformation. It is the only company to receive this award.

Tanate Kasemsarn, Head of ESG, KPMG in Thailand

Tanate Kasemsarn, Head of ESG, KPMG in Thailand Ganesan Kolandevelu, Head of Climate Change and Sustainability Services, KPMG in Thailand

Ganesan Kolandevelu, Head of Climate Change and Sustainability Services, KPMG in Thailand Natthaphong Tantichattanon, Partner, Climate Change and Sustainability Services, KPMG in Thailand.

Natthaphong Tantichattanon, Partner, Climate Change and Sustainability Services, KPMG in Thailand.

Thailand Prime Minister Meets Huawei CEO to Promote Collaboration on Digital Transformation and Talent Development

Thailand Prime Minister Meets Huawei CEO to Promote Collaboration on Digital Transformation and Talent Development Thailand Prime Minister Meets Huawei CEO to Promote Collaboration on Digital Transformation and Talent Development

Thailand Prime Minister Meets Huawei CEO to Promote Collaboration on Digital Transformation and Talent Development