The Thai National Shippers’ Council projects a brighter outlook in the export of textiles, garment and machinery this year, the council’s vice chairman Visit Limluecha said.

The council classified products under three categories: V or double-digit growth; U or single-digit growth; and L or no growth or contraction.

Industries in the V-growth group include textile and garment, machinery, finished oil and rice. Double-digit growth is expected for these products because they showed low contraction late last year.

The garment and textile sector dropped 18 per cent last year, while machinery and machine equipment fell 9.2 per cent.

Meanwhile, U-shaped growth is expected for automotive and component parts, electric and electronics appliance, food, rubber, cassava and jewellery and gems.

No growth or L-shaped growth is expected for industries like sugar, plastic pellets and products made of plastic pellets.

He said this is because major sugar producers like Brazil have released massive amounts of sugar and alcohol, causing a glut in the global market.

The council has forecast that sugar exports will suffer a drop of between 7 and 10 per cent, the same as in 2020.

Visit added that the Covid-19 pandemic will still be a key factor in affecting industries globally, especially in relation to luxury items, though market competition will intensify if manufacturers launch promotions.

Construction of Phuket highway will kick off by 2023: Transport Ministry

EconJan 11. 2021Transport Minister Saksayam Chidchob

By The Nation

The construction of the Muang Mai-Koh Kaew Highway should begin by 2023, Transport Minister Saksayam Chidchob said.

The 22.4-kilometre highway, which is part of the ministry’s project to ease traffic in Phuket, will link Phuket airport with Krabi and Phang Nga.

The design and environmental impact assessment for the highway has been completed, he said, adding that the construction is expected to cost Bt11.5 million, plus Bt11.1 billion for land reclamation.

The Highways Department believes the highway will be ready by 2025.

The Public-Private Partnership Committee has called on state agencies to speed up the development of 18 top-priority mega-projects worth Bt472 billion as part of the government’s efforts to drive the economy this year.

The committee is chaired by Deputy PM Supattanapong Punmeechaow.

Meanwhile, Transport Minister Saksayam Chidchob said the ministry has already asked related agencies like the National Economic and Social Development Council for their opinions on its many projects.

He added that the State Railway of Thailand is expected to call bids for the Tao Poon-Ratburana Purple Line mass transit route in the next quarter.

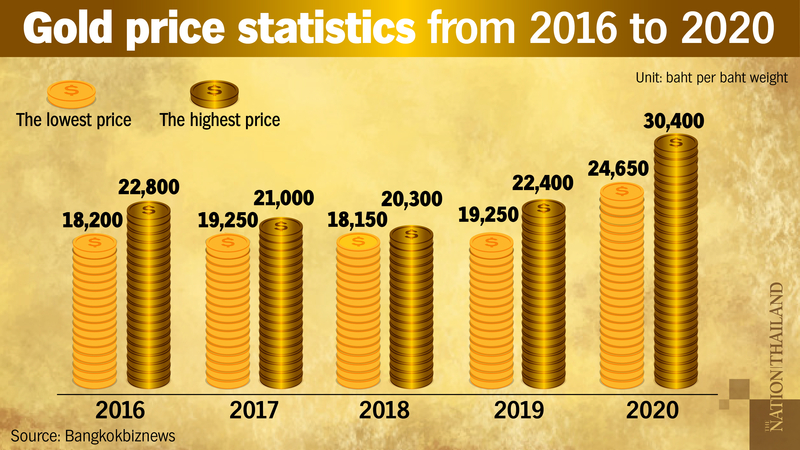

Gold price is expected to hit a new high this year, with experts predicting it could surpass the Bt30,400 per baht weight it touched in 2020.

MTS Gold chief executive Nattapong Hirunyasiri said the price is currently moving in positive territory as its returns as of January 5 this year were 3 per cent despite the news of Covid-19 vaccines.

In the long term, he expected funds to flow into the gold market due to increasing inflation rate, low-interest rate and US President-elect Joe Biden’s policies and measures to inject cash into the economic system.

“However, the gold price would move at around Bt28,000 per baht weight in the short term due to the baht’s appreciation. Meanwhile, returns on gold this year are expected to be at 25 per cent compared to 30 per cent last year,” he said.

Pawan Navawattanasap, YLG Bullion International chief executive officer, expected gold price to move in positive territory in the long term as SPDR funds had bought back gold at the end of last year.

She said gold price had gained positive sentiment from rising Covid-19 cases and the weakening US dollar, adding that foreign strategists predicted the dollar this year would weaken further.

“We expect gold price to move in positive territory for up to two years as the interest rate is expected to remain at a low level until 2023,” she said.

She added that the price could hit US$2,000 if it can pass the resistance line at $1,965 per ounce.

“Investors who are able to tolerate risks can buy gold when the price drops to $1,921 per ounce and set up stop-loss point at $1,907 per ounce,” she added.

The chief of state think-tank, National Economic and Social Development Council (NESDC), expressed concerns about the impact of the new wave of Covid-19 infections, saying this outbreak may hit the economy harder if steps are not taken in time.

In an exclusive interview with Krungthep Turakij newspaper, NESDC secretary-general Danucha Pichayanan said that though some countries have started mass vaccinations, it will still take a long time for inoculations to arrive in every corner of the world.

And while Thailand waits for vaccines to arrive, the renewed outbreak could worsen and hit the economy hard.

The new round of infections originated in Samut Sakhon province to the west of Bangkok, and spread quickly, forcing authorities to impose restrictions on 28 provinces.

He said if the virus can be contained by early February, then the government will not have to change its economic management plans and should be able to announce relief packages in the next few weeks.

He added that so far, this new outbreak has not had as severe an impact on the economy as the first round of infections did last year. This is because many economic activities have been conducted to some extent, like people moving around and restaurants remaining open, he said.

Also, he added, Thailand is better prepared this time around and has ensured there is adequate supply of face masks, medical equipment and medication.

“Managing the economy in the first six months of this year is being challenged by the new outbreak. We have to contain it and ensure everyone’s safety first before we can drive the economy forward. And if we are successful in containing the outbreak, then we will draw more foreign investment,” he said.

However, he said, apart from Covid-19, there are more risks that need to be managed.

The first is ensuring people keep their jobs and for this we have to help bolster businesses while the economy gradually recovers from the Covid-19 fallout, he said.

The second is high household debt, which currently stands at 83 per cent of the gross domestic product. The country must address both short- and long-term issues related to debt, and ensure people are financially literate.

The third is the appreciation of the baht, which has had an adverse impact on exports. A drop in the import of capital goods and limited overseas investments by Thai corporations have contributed to the strength of the baht. We need to ensure the stronger baht does not disrupt economic recovery, he said.

Another important factor is US President-elect Joe Biden’s policies once he takes over from President Donald Trump on January 20. Thailand has to wait and see which direction Biden’s policies take. For instance, he said, the US-China trade war is expected to continue and Biden may come up with policies that have an impact on Thailand and the global economy.

The government also needs to focus on the low-income group in the first half of 2021 and find ways to boost domestic consumption. Also, he said, the economy will rely on private investment and public spending, such as Bt400 billion in government loans aimed to lift the grassroots economy in the first six months.

“In a move to sustain economic growth, the Government Centre for Economic Situation Administration will also boost foreign direct investment, which we expect will flow into the country in the fourth quarter of the year,” he said.

The country plans to restructure the economy so it has a stronger base for the next four to five years, and in order to do this, investment is required in key industries such as electric vehicles, battery, charging stations, electrical grids and electric systems, sensors and electronics.

If Thailand wants to achieve its aspiration of becoming a medical hub, then it also needs to invest in human capital and develop research centres.

The Board of Investment (BoI) also needs to adapt its strategy so it draws investment from the world’s top five or 10 firms.

Government agencies and BoI have discussed the options of investment incentives and technology transfer, which should draw more investment in the fourth quarter. This will lead to a new industry cluster and a production base in the long-term, he said.

If Thailand manages to effectively contain the spread of the virus, the economy should grow 4 per cent this year, he said, citing NESDC’s forecast.

“The Covid-induced crisis has also created an opportunity for economic restructuring, which can become a springboard for robust future growth,” he added.

The 26 initial public offerings (IPOs) on the Thai stock market last year saw average returns of 48.72 per cent at close of first-day trading, Bangkokbiznews revealed on Friday.

However, seven of the 26 new listings – four on the Stock Exchange of Thailand (SET) and three on the Market for Alternative Investment (MAI) – saw their IPO price drop below the subscription price.

Currently, 12 of the companies have allocated their IPO shares, namely Next Capital (NCAP), Well Graded Engineering (WEG), Dhouse Pattana (DHOUSE), Siam Rajathanee (SO), K&K Superstore Southern (KK), Sirakorn (SK), Micro Leasing (MICRO), Earth Tech Environment (ETC), I&I Group (IIG) Silicon Craft Technology (SICI), Sri Trang Gloves Thailand (STGT), Central Retail Corporation (CRC), NR Instant Produce (NRF) and Yggdrazil Group (YGG).

The top five investors who obtained most IPO shares are as follows:

1. Wichai Wachiraphong: 51.67 million shares from five companies – DHOUSE (5 million shares) MICRO (2.29 million), ETC (18 million), STGT (22.20 million) and NRF (4.18 million)

2. Ratchayut Jeerapornprapa: 28.15 million shares from two companies, – ETC (25.65 million) and DHOUSE (2.5 million)

3. Annop Limprasert: 27.06 million shares from two companies, namely ETC (24 million) and MICRO (3.06 million)

4. Komol Juangroongruangkit: 26.06 million shares from two companies, namely ETC (25 million) and SICT (1.06 million)

5. Sippakorn Kaosa-ard: 23 million ETC shares.

Meanwhile, the top five IPO investors in terms of profit netted more than Bt1.4 billion in total at close of first-day trading.

The top five were Wichai Wachiraphong (Bt602.99 million), Katreeya Beaver (Bt432.53 million), Chawin Tangkaravakoon (Bt141.51 million), Kanes Tangkaravakoon (Bt139.39 million) and Aiyawatt Srivaddhanaprabha (Bt106.29 million).

Exporting the U.S. shale boom has changed oil markets forever

EconJan 10. 2021A Chevron sign in front of a horizontal drilling rig on federal land in Lea County, N.M., on Sept. 10, 2020. MUST CREDIT: Bloomberg photo by Callaghan O’Hare.

By Syndication Washington Post, Bloomberg · Sheela Tobben, Dave Merrill · BUSINESS, US-GLOBAL-MARKETS

Five years ago on New Year’s Eve, the Theo T left the Texas Gulf Coast with the first U.S. shale crude shipment overseas. The oil, gathered from nearby ConocoPhillips wells and sold to trading giant Vitol Group, set sail for Italy just two weeks after lawmakers lifted a long-standing ban on exports.

It was the start of a trade that would reshape global oil markets, shift geopolitical power and upend entire economies.

The shale boom itself has turned the U.S. into the world’s largest oil producer and has moved it ever closer to a long-cherished dream of ending dependence on Middle East oil. But the export boom created an entirely new market, sending crude pulled from the shale fields of Texas, New Mexico and North Dakota to more than 50 countries, with shipments often surpassing those of any OPEC nation aside from Saudi Arabia.

These past five years could very well go down as the best years that U.S. shale oil exporters will ever see. Covid-19 has obliterated global fuel demand and bankrupted more than 40 drillers across America. Exactly how much oil leaves U.S. shores in the coming years will largely depend on how quickly the world can recover from the pandemic and how aggressively politicians work to shift the world away from fossil fuels.

But the global reach of U.S. shale has changed oil markets for good and remains a potent, diplomatic weapon for the U.S.”Opening the shale revolution to the world through the export ban lifting helped shift the global oil market psychology from supply scarcity to abundance,” said Karim Fawaz, director of research and analysis for energy at IHS Markit. “It unshackled the U.S. industry to keep growing past its domestic refining limitations.”

Perhaps no two groups have gained from the export of America’s shale boom more than producers of U.S. oil and the giant commodities merchants who trade it. Wildcatters including billionaire Harold Hamm of Continental Resources Inc. and Scott Sheffield of Pioneer Natural Resources Co. saw their revenues more than double as exports took off. “Today the U.S. has its own petrodollars,” Hamm said in August 2018 as U.S. oil shipments overseas boomed.

Trading giants including Trafigura Group, Vitol, Gunvor Group and Mercuria Energy Group profited from buying cheaper shale oil, shuttling it to the U.S. coast and shipping it to eager buyers in Europe and Asia. Betting that shipments would surge, they expanded their trading desks in the U.S., invested in ports, pipelines and export facilities. By the last week of 2019, exports of American oil had reached nearly 4.5 million barrels a day.

U.S. shale’s gain was OPEC’s loss. As shale oil flooded the market, OPEC was forced to cede market share. The U.S., which had been one of OPEC’s biggest customers, has cut its monthly imports by about 50% since mid-2006. Recently, Saudi Arabian cargoes to the U.S. fell to zero for the first time since at least 2010.

Exports have turned U.S. shale into a permanent thorn in OPEC’s side. The oil cartel has had to join forces with Russia, Mexico and other major producers to ratchet back production several times in the past five years while U.S. shale expanded its reach into key markets.

Shale now shares the fortunes – and the misfortunes – of being a major exporter. The strongest evidence of this yet came in March when U.S. President Donald Trump joined leaders of the world’s largest oil-producing nations to hammer out an unprecedented accord to save oil markets from total collapse as the pandemic slashed demand.

The U.S.’s shrinking dependence on foreign imports has also allowed the Trump administration to impose increasingly debilitating sanctions on two OPEC founding members – Venezuela and Iran – without fear of higher fuel prices back home. And with American shale now readily available in global markets, oil price spikes tied to conflicts in the Middle East are shorter and more subdued.

“The flow of U.S. oil since the ban’s end has kept global oil supply in balance even at times when politics have caused the loss of supply from Iran, Venezuela and Libya,” said Sandy Fielden, director of oil research at Morningstar Inc.

How long the U.S. can maintain this clout on global oil markets remains to be seen.

One bullish sign for U.S. oil exports: China’s appetite for crude has come back with a vengeance since the country emerged from lockdowns. That has helped draw down American oil inventories as U.S. cargoes start hitting the water once again, reaching 3.6 million barrels a day in the week of Christmas.

There is no other country that will dictate the fate of U.S. oil exports more than China. About two years after U.S. lawmakers lifted the export ban, shipments to China reached 2 million barrels a day, making it by far the largest buyer of American oil. The Asian nation’s appetite for crude has rebounded since it emerged from lockdowns, but Saudi Arabia and Russia remain major suppliers to the country and competition may heat up later this year as OPEC+ restores output.”The Asian market will become more competitive as OPEC+ restores some of its production,” said Shirin Lakhani, a senior oil analyst at Rapidan Energy Group. “For OPEC+ producers, sales into Asia have the best profit margins due to proximity and logistics.”

Demand for U.S. barrels will also depend on how well the global economy fares in the coming years after its deepest recession since World War II. The World Bank forecasts a 4% economic rebound this year, following a 4.3% contraction in 2020, but cautioned there’s an “exceptional level of uncertainty” as the pandemic may reduce potential global growth for a decade. It will take until the end of 2021 for the oil glut left behind by the pandemic to clear as demand will be “lower for longer than expected” when the virus emerged in the spring, the International Energy Agency said in December.

The incoming Biden administration and its plan to completely reshape U.S. energy policy will undoubtedly affect U.S. oil exports. Among the president-elect’s promises on the campaign trail were stronger regulation of the hydraulic fracturing that unleashed the U.S. shale boom, a ban on fracking federal lands and a broader transition away from fossil fuels. Depending on how it’s executed, the ban alone may not significantly affect U.S. oil shipments. It would theoretically only apply to new drilling licenses and affect a fairly limited amount of new oil output, namely in New Mexico.

But that may only prove to be a temporary boon for oil exporters. Joe Biden is among a growing chorus of world leaders pledging to wean their nations off fossil fuels for good. More than 120 countries, including China, the U.K. and Canada, have committed to achieving net-zero emissions over the course of the next three decades. The president-elect himself has pledged to achieve net-zero emissions in the U.S. no later than 2050. Electric transportation lies at the center of virtually every country’s plan to go carbon-neutral.

Annual sales of electric cars around the world – including trucks and buses – reached almost 27 million in 2019 and are set to accelerate in the coming years to a rate of 133 million vehicles a year in the next two decades, according to BloombergNEF estimates. By 2040, around 500 million passenger electric vehicles will be on the road, or roughly one third of the world’s total.But as long as the world moves mostly on fossil fuels, shale will continue to fight for its share of the global market. “The lifting of the export ban and the incredible growth and resilience in domestic shale will keep the U.S. a crucial exporter of American crude oil for the foreseeable future,” Lakhani said.

Return to food protectionism is riling farmers in Argentina

EconJan 10. 2021Alberto Fernandez, then Argentina’s president-elect, leaves from a news conference following a meeting with Andres Manuel Lopez Obrador, Mexico’s president, in Mexico City on Nov. 4, 2019. MUST CREDIT: Bloomberg photo by Alejandro Cegarra.

By Syndication Washington Post, Bloomberg · Jonathan Gilbert · BUSINESS, WORLD, US-GLOBAL-MARKETS, THE-AMERICAS

A ban on corn exports in Argentina is fanning fear among farmers and traders that one of the world’s top food suppliers is returning to an era of brutal meddling in crop markets.

The measure creates yet another driver for surging global grain futures, given Argentina is the third-largest shipper of corn, and stokes concern of an up-tick in food nationalism around the world as the pandemic disrupts trade.

The Argentine government suspended corn shipments through February to force growers to sell to the local livestock industry. The idea is to suppress feed costs and, in turn, prices of beef, pork, chicken, eggs and milk in a country where inflation is forecast to reach 50% this year.

In protest, three of Argentina’s four main farm associations have told members to halt trading between Jan. 11 and Jan. 13, adding to industry unrest as port workers strike over pay. But President Alberto Fernandez is standing firm, saying on radio Wednesday that food prices at home need to be decoupled from export values that are on a tear.

Argentine farmers have grappled with this sort of intervention before and ultimately, they say, it’s counterproductive — curbing investment and planting, and eventually causing shortages. They’re worried about the ban being extended, both in time and to other products like wheat and beef.

That’s because the last time the Peronist party was in power — for a stretch over the previous two decades — exports were restricted by trade barriers, taxes or outright bans. Production dwindled, only bouncing back under Mauricio Macri, the market-oriented president voted out a year ago.

“Pulling back on production is our defense mechanism,” said Luis Garmendia, a farmer in the town of Intendente Alvear, who planted 95 hectares (235 acres) of corn this season.

Since the government announced the export suspension on Dec. 30, Chicago futures have advanced more than 3%, extending gains in the past six months to 43%. Global crop prices are surging as investors turn to commodities amid a weakening dollar; dry South American weather dims supply prospects; and China rebuilds its hog herd that was devastated by African swine fever.

Last month, Russia formalized plans to introduce a wheat-export tax and grains quota in response to President Vladimir Putin’s call to cool food-price inflation.

Argentina’s Agriculture Ministry declined to comment on the possibility of further export limits. To be sure, when the government hiked taxes on shipments days after taking office in late 2019, the increases for grains and beef were less than expected and sales abroad have stayed at Macri-era levels.

But exporters warn that could change swiftly.

“Intervention in transparent markets creates uncertainty among farmers who delay sales and cut back planting,” crop export group Ciara-Cec, whose members include the powerhouses of agricultural trading, said in a statement.

Farmer Garmendia is already considering abandoning wheat planting later in the year.

The agriculture industry has every right to be perturbed after Cristina Kirchner, the former president and foe to farmers who’s now wielding influence as deputy leader, anticipated the president’s remarks on radio by calling last month for “accessible food prices,” said Pablo Adreani, an agribusiness consultant in Buenos Aires.

It’s a balancing act for the government that’s akin to a game of whac-a-mole. President Fernandez and Vice President Kirchner want to rein in inflation that has stayed above 35% for more than two years to help their base of poorer people. But food protectionism jeopardizes the farm-export dollars that Argentina desperately needs for currency and economic stability.

The leadership duo also knows the stakes of getting into a fight with farmers after widespread protests in 2008 over a move to hike taxes rattled Kirchner’s government. Alberto Fernandez was cabinet chief at the time.

In any case, it’s unclear whether the protectionist measures will work as a tool to stem food inflation, said Abdolreza Abbassian, a senior economist at the United Nation’s Food and Agriculture Organization.

Under Fernandez, Argentina had already been meddling in agriculture markets, tweaking soybean taxes to try to boost exports; fiddling with wheat values to squeeze tax revenues higher; and capping beef prices.

As things stand, Argentine grain and cattle markets aren’t facing anything like the heavy-handed intervention of the Kirchner period. But should there be a repeat scenario, global crop traders will take note because farmers would respond by ditching rotation strategies in favor of soy mono-culture, said Eugenio Irazuegui, head of research at grains brokerage Enrique Zeni in Rosario.

Even under Kirchner, soybeans were exported freely because they have little impact on domestic food prices given soy isn’t a staple in Argentina, and shipments of the oilseed provide an indispensable gush of tax revenue.

Expectations for more soy planting in Argentina, which is the world’s biggest exporter of processed soy meal used as hog feed, could cap a rally for the tight global meal market.

Krungsri Foundation donates blankets as cold weather settles in

Jan 08. 2021

By The Nation

Krungsri Foundation, led by its assistant secretary Poonsit Wongthawatchai (pictured 2nd left), recently donated 500 blankets to help people in remote areas during this period of cold weather.

The blankets were donated to the “Thai PBS and Networks Spread Warmth to Needy People in Chaloemprakiat District, Nan, 2020” project, represented by Thaipbs Foundation manager Khaisaeng Sakda, (3rd left).

Companies that backed Trump for years are facing a reckoning after the attack on the Capitol

CorporateJan 09. 2021A statue of Zachary Taylor was defaced at the U.S. Capitol after Trump supporters breached the U.S. Capitol Jan. 7, 2021, in Washington, D.C. MUST CREDIT: Washington Post photo by Katherine Frey

By The Washington Post · Todd C. Frankel, Jeff Stein, Jena McGregor, Jonathan O’Connell · NATIONAL, BUSINESS, POLITICS

The bargain with the business world worked like this: They mostly tolerated President Donald Trump’s sometimes outrageous behavior in exchange for business-friendly corporate tax cuts and regulatory rollbacks, deals they celebrated over Oval Office handshakes.

But that arrangement started to sour in the last year with the Trump’s administration’s missteps on the pandemic and Black Lives Matter protests before swiftly deteriorating in recent days with a mob assault on the Capitol prodded on by the president. That led the National Association of Manufacturers – comprised of exactly the kind of companies he considered key to his “Make America Great Again” mission – to call for Trump’s immediate removal from office for actions by the pro-Trump mob described as “sedition.”

The message was not the typical corporate condemnation. It was something the trade group of 14,000 companies – which usually avoids politics – never before imagined issuing.

“It was a clear and present danger to our democracy,” said Jay Timmons, the group’s president. “And we couldn’t stand for that. That transcended everything.”

Business groups big and small largely stuck by Trump as he broke one norm after another over the past four years, including insulting immigrants, appearing to empathize with White supremacists in Charlottesville, Va., and clearing a Black Lives Matter protest in Washington for a photo op. They stuck by him still after he threatened the Ukrainian prime minister to help his election chances, after his impeachment, after he intentionally downplayed the effects of the coronavirus and last week after he was recorded pressuring the Georgia Secretary of State to overturn election results.

The once-comfortable alliance between Trump and Corporate America has shown unprecedented strain since Wednesday’s attack, forcing a re-examination of everything that businesses had won over the last four years from a White House now thrown into chaos.

Following the attack on the Capitol, advisers crucial to the president’s economic policies tried to distance themselves from the Trump-induced mayhem. Some resigned, such as former chief of staff Mick Mulvaney, who was serving as envoy to Northern Ireland, explaining to CNBC that, “we signed up for lower taxes and less regulation.” Companies considered cutting off the money spigot to the politicians seen as fomenting the worst of it. Firms that did business with theTrump family were re-examining the cost of being associated with a historic insurrection.

Yet some officials sought to maintain a neat separation between Trump’s economic policies and what had occurred at the Capitol.

“It isn’t going to affect tax rates. How about monetary policy? Allow me to stay pure to my turf,” Art Laffer, a supply side economist who is close with White House economic officials and speaks to the president, said in a brief interview.

But there remained plenty of criticism for the business world’s willingness to go along with Trump for so long.

“Their attitude was: ‘Let’s take the big tax cuts and hold our noses for the obvious xenophobia and authoritarianism.’ It was a classic Faustian bargain,'” said Rep. Brendan Boyle, D-Pa., a member of the House Ways & Means Committee. “They should have known from the beginning.”

The economy provided Trump with cover after he previously ran into trouble, such as for his “very fine people on both sides” comment following the Charlottesville clashes and his administration’s defense of the images of “kids in cages” along the southern U.S. border.

Many companies abandoned the various policy councils set up by the White House as a result. Others issued statements. But little was different.

Events of the last year seemed to change those corporate calculations for some groups, including by the National Association of Manufacturers.

The trade group had worked closely with the Trump administration on tax reform and regulatory issues. When Timmons, the group’s president, visited the White House in March 2017, he told Trump that manufacturers increasingly felt the country was on the right track.

“And that’s because of the focus on taxes, regulations, infrastructure investment,” Timmons said, according to a meeting transcript. “We appreciate your commitment to investment in job creation and manufacturing. And we’re going to deliver.”

But everything changed when Vice President Mike Pence delivered a speech last February at the manufacturing group’s board meeting, where he seemed to downplay the threat posed by a then-still novel coronavirus, according to three senior leaders.

That was followed by the nation’s problems with personal protective equipment and ventilators. Manufacturers struggled to figure out how to help, stymied by a chaotic federal response. The trade group launched its own “wear a mask” ad campaign while Trump and other Republicans continued to cast doubt on facemasks. The group condemned the death of George Floyd over the summer. And after the election, it called on Trump’s administration to provide help to President-elect Joseph Biden’s transition team.

But the scenes from Wednesday were the breaking point. Senior leaders quickly drafted a statement – while police were still trying to clear the Capitol – calling on Trump to be removed from office and pointing a finger at any politician involved in doubting election results.

“The outgoing president incited violence in an attempt to retain power, and any elected leader defending him is violating their oath to the Constitution and rejecting democracy in favor of anarchy,” said the statement from Timmons.

The manufacturers were not unanimous in supporting Timmons’ stance.

Chuck Wetherington, a member of the executive committee and president of BTE Technologies in Hanover, Md., said the group and Trump had increasing differences over trade, immigration and racism. He said he was proud of Timmons’s courage in making the statement.

“What we saw Wednesday was democracy under attack,” he said.

But another member of the executive committee, Steve Straub, president of a Dayton, Ohio metal fabrication supplier, said in an email he didn’t support the statement. “There are other board members who feel the same way,” he said. He continued displaying a photo of him alongside Trump on his company website.

Other companies and business groups issued various statements, among them the U.S. Chamber of Commerce, the heads of financial giants Citi and J.P. Morgan. The Business Roundtable, a group representing the nation’s most powerful chief executives, said in a statement to The Washington Post that because of the falsehoods from politicians about the election outcome “many of our companies are evaluating their contributions.”

None of the groups went as far as the manufacturing group.

The stance was starker than the ones taken by several of the corporations on the manufacturing group’s executive committee. Some failed to mention Trump’s name. Others offered general calls for unity.

In an email to employees, Caterpillar’s chief executive, Jim Umpleby, said: “We watched in disbelief as protestors broke through security barricades” and strongly condemned “the resulting chaos, destruction and loss of life” but did not mention Trump’s role in the events.

Ted Doheny, president of packaging firm Sealed Air, said in an emailed statement to The Washington Post that he condemned the violence and “I stand with others in the business community who are calling for unity and a smooth transition of power.”

Another large company on the manufacturing group’s executive committee, Emerson Electric, did not respond to a request for comment. According to the Center for Responsive Politics’ Open Secrets website, the St. Louis-based company gave individual and PAC contributions totaling $51,900 to the campaign of Sen. Josh Hawley, R-Mo., one of the lawmakers who voted to object to certifying election results.

Emerson’s CEO, David Farr, gave Trump Victory – a committee raising money for Trump’s reelection and the Republican party – $100,000 in 2020, according to Federal Elections Commission data. Spokesman David Baldridge said in an email that Farr was not available for an interview and the company declined comment.

The flood of corporate statements was the result of companies suddenly finding themselves in the strange position of needing to defend democracy.

“They spoke out because overturning an election is not simply a threat to our political system,” said Ronnie Chatterji, a business professor at Duke University and former economic advisor to President Obama. “The rule of law that ensures peaceful transitions of power also makes business possible.”

A major outstanding question is whether executives or political action committees affiliated with companies will reduce their donations to GOP candidates who supported Trump’s efforts to overturn the election and incite violence.

Some companies have asked about the pressure to stop political contributions to congressional members who voted against certifying the election, said Nick DeSarno, director of digital and policy communications for the trade group of policy officials at large corporations and advocacy groups.

“Companies are actively considering if these lawmakers will be supported by their PAC in the future,” DeSarno said.

Bruce Haynes, chairman of Sard Verbinen & Co.’s public affairs group, said his firm has been contacted by clients trying to determine whether they should make a statement amid this week’s turmoil, and if so, what should be said.

“Nothing like this has ever happened before,” Haynes said. “It’s not in the playbook.”

Haynes said it is too early to know, but he expected companies to have to look harder at their political donations and relationships.

“I’d say that scrutiny is about to rise significantly,” he said.

One major union group that had supported Republican lawmakers on matters such as project labor agreements had also decided to cut ties with Republicans who voted against the vote certification, according to one labor official granted anonymity to discuss the private matter.

More than half of the 33 chief executives gathered on a virtual call this week said they would reconsider investments in states where elected officials are impeding an orderly presidential succession, said Yale School of Management’s Chief Executive Leadership Institute founder Jeffrey Sonnenfeld, who organized the call.

Sonnenfeld, who argued CEOs have opposed the Trump administration at times throughout his term, including on environmental regulatory rollbacks and immigration issues, said he believed companies would be limiting contributions to lawmakers who denied election results in the future. But others were skeptical about a major shift in lobbying and campaign contributions.

While companies may face pressure to change, Chatterji said, “I do not think it will happen.”

The costs of the Capitol insurrection have been felt inside the White House. Tyler Goodspeed, acting chair of the White House Council of Economic Advisers, submitted his resignation a day after the storming of the Capitol. His departure means there are no remaining members of the White House Council of Economic Advisers.

Several senior White House officials called outside advisers Wednesday weighing whether they should also depart the administration amid a broader exodus of senior White House officials, according to three people granted anonymity to share details of private conversations.

But even those who have not cut ties to the White House’s economics team are worried.

“It’s a disaster. It’s been a disaster. My main concern as a policy guy is that this tarnishes his economic achievements, that’s my main concern right now,” said Stephen Moore, a longtime White House economic adviser and conservative.

It’s also unclear if fallout from the Capitol melee will have a major effect on Trump and his business when he leaves office.

Shopify, the company that runs online stores for the Trump Organization and the Trump campaign, pulled down both sites Thursday. It issued a statement saying the company “does not tolerate actions that incite violence.” Trump earned $930,869 in income from his company’s site in 2019, according to his most recent government disclosure. Shopify’s decision was first reported by the Wall Street Journal.

JLL, the real estate services firm that the Trump Organization hired in a failed attempt to sell his D.C. hotel lease, told The Washington Post on Friday that it will no longer be helping Trump with the sale.

“Our previous listing agreement with the Trump Organization to sell its hotel in Washington D.C. has expired and we are no longer doing business with them,” said spokesman Jesse Tron in a statement.

Lawyers are abandoning Trump, too, for the challenge to the election results and what they view as his role in the riot. The most recent came from Philadelphia attorney Jerome M. Marcus, who filed a motion in federal court Thursday withdrawing from the case. “The client has used the lawyer’s services to perpetrate a crime,” the motion states.

But any impact on companies could be fleeting.

On Wednesday, pro-Trump insurrectionists still occupied the Capitol building. The emergency had not waned. A peaceful transfer of power remained in doubt.

Transport Minister Saksayam Chidchob

Transport Minister Saksayam Chidchob Deputy PM Supattanapong Punmeechaow

Deputy PM Supattanapong Punmeechaow

A Chevron sign in front of a horizontal drilling rig on federal land in Lea County, N.M., on Sept. 10, 2020. MUST CREDIT: Bloomberg photo by Callaghan O’Hare.

A Chevron sign in front of a horizontal drilling rig on federal land in Lea County, N.M., on Sept. 10, 2020. MUST CREDIT: Bloomberg photo by Callaghan O’Hare. Alberto Fernandez, then Argentina’s president-elect, leaves from a news conference following a meeting with Andres Manuel Lopez Obrador, Mexico’s president, in Mexico City on Nov. 4, 2019. MUST CREDIT: Bloomberg photo by Alejandro Cegarra.

Alberto Fernandez, then Argentina’s president-elect, leaves from a news conference following a meeting with Andres Manuel Lopez Obrador, Mexico’s president, in Mexico City on Nov. 4, 2019. MUST CREDIT: Bloomberg photo by Alejandro Cegarra.

A statue of Zachary Taylor was defaced at the U.S. Capitol after Trump supporters breached the U.S. Capitol Jan. 7, 2021, in Washington, D.C. MUST CREDIT: Washington Post photo by Katherine Frey

A statue of Zachary Taylor was defaced at the U.S. Capitol after Trump supporters breached the U.S. Capitol Jan. 7, 2021, in Washington, D.C. MUST CREDIT: Washington Post photo by Katherine Frey